Students can access the CBSE Sample Papers for Class 11 Accountancy with Solutions and marking scheme Set 3 will help students in understanding the difficulty level of the exam.

CBSE Sample Papers for Class 11 Accountancy Set 3 with Solutions

Time Allowed : 3 hours

Maximum Marks: 70

General Instructions:

- This question paper contains 34 questions. All questions are compulsory.

- This question paper is divided into two parts, Part A and B.

- Question Nos. 1 to 15 and 25 to 29 carries 1 mark each.

- Questions Nos. 16 to 18,30 to 32 carries 3 marks each.

- Questions Nos. 19,20 and 33 carries 4 marks each

- Questions Nos. from 21 to 24 and 34 carries 6 marks each

- There is no overall choice. However, an internal choice has been provided in 7 questions of one mark, 2 questions of three marks, 1 question of four marks and 2 questions of six marks

Part – A ((Financial Accounting – I)

Question 1.

Which accounting helps to ascertain the cost of production and to provide useful costing information to the management for decision making?

(A) Management Accounting

(B) Cost Accounting

(C) Both (A) and (B)

(D) None of the these [1]

Answer:

(B) Cost Accounting

Question 2.

Assertion: The main function of financial accounting is the preparation of financial reports which provide summary of a firm’s financial condition.

Reason: Income Statement or Profit & Loss Account and Balance Sheet are the end products of financial accounting.

(A) Both A and R are corred, and R is the correct explanation of A.

(B) Both A and R are correct, but R is not the correct explanation of A.

(C) A is correct, but R is incorrect.

(D) A is incorrect, but R is correct. [1]

Answer:

(B) Both A and R are correct, but R is not the correct explanation of A.

Question 3.

Assets is of the following types:

(A) Fixed

(B) Fictitious

(C) Current

(D) All of the these

OR

Give an example of capital receipt.

(A) issue of shares

(B) Repairs to furniture

(C) Wages paid to regular workers

(D) Purchase of furniture. [1]

Answer:

(D) All of the these

OR

(A) issue of shares

Explanation: Issue of shares will increase the capital of the company and is non-recurrent in nature. Thus, it is a capital receipt.

Question 4.

Which of the following errors do not affect the trial balance?

(A) Errors of principle

(B) Compensating errors

(C) Errors in carrying forward

(D) Both (A) and (B) [1]

OR

Which of the following errors affect the trial balance:

(A) Errors in posting

(B) Errors in carrying forward

(C) Both (A) and (B)

(D) None of the these [1]

Answer:

(D) Both (A) and (B)

Explanation: Error of Principle: This error happens because accounting is not in accordance with accounting principles and standards.

Compensating Error: Compensating error refers to a situation when an accountant makes mistakes on both sides of an account, hence compensating one error for another.

OR

(C) Both (A) and (B)

Explanation : Error of Posting: Error of posting arises when a transaction is correctly recorded in the books of original entry including journal but posted wrongly in ledger accounts. Error of Carrying Forward: Error in carrying forward arises when a mistake occurs in carrying forward a total from one page to the next page.

Question 5.

……………. is an accounting practice of manipulating the business results, usually to show a respectable figure of profits more than the real profits.

(A) Window Dressing

(B) Bridging

(C) Wmdow Changing

(D) None of the these [1]

Answer:

(A) Window Dressing

Explanation: Window dressing is an accounting practice of manipulating the business results, usually to show a respectable figure of profits more than the real profits. The practice may be followed by loss making companies to show a profit. For this purpose, companies may not show some expenses or the expenses may be shown less. On the other hand, income may be more than the actual. Firm may show inventories at higher value (over valuation of stock) and may hide bad debts written off during the year.

Question 6.

Pick the odd one out:

(A) GST

(B) Custom Duty

(C) Sales Tax

(D) Income Tax [1]

OR

Consider the following statements:

(i) Accounting standards are the norms of accounting policies and practices to be adopted by the accountants.

(ii) Accounting standards make accounting procedures universally acceptable by removing the diverse accounting

practices and policies.

(iii) Accounting standards serve as a guide for solving one or more accounting problems.

(iv) Accounting standards provide the basis upon which financial statements are prepared.

Identify the correct statement/s which state the nature of accounting standards.

(A) (i), (iii) and (iv)

(B) (ii), (iii) and (iv)

(C) (i), (ii), (iii) and (iv)

(D) (i), (ii) and (iii)

Answer:

(D) Income Tax

Explanation: Income tax is a direct tax whereas the rest are indirect taxes.

OR

(C) (i), (ii), (iii) and (iv)

Question 7.

Assertion: Under cash basis of accounting the expenses and revenues are recorded when the transaction is done

and not when the amount is actually received.

Reason: Cash Basis of Accounting does not distinguish between capital and revenue expenditure, making

comparisons between two years inconsistent and impractical.

(A) Both A and R are correct, and R is the correct explanation of A.

(B) Both A and R are correct, but R is not the correct explanation of A.

(C) A is correct, but R is incorrect.

(D) A is incorrect, but R is correct. [1]

Answer:

(D) A is incorrect, but R is correct.

Explanation: Under cash basis of accounting, expenses and revenues are recorded when actual cash is paid or received.

Question 8.

Consider the following statements with regard to the need for preparing the Bank Reconciliation Statement:

(i) It helps the management in checking the accuracy of entries recorded in Cash Book

(ii) It helps in keeping track of cheques, etc., sent to the bank for collection. Any undue delay in the clearance of

cheques can be noticed.

(iii) It helps in bringing out any errors that may have been committed either in cash book or in the pass book.

Identify the correct statement/statements:

(A) (i) and (iii)

(B) (ii) and (iii)

(C) (i), (ii) and (iii)

(D) (i) only [1]

OR

…………….. means a detail of bank account as shown by the bank records.

(A) Pass Book

(B) Cash Book

(C) Cheque Book

(D) Bank Reconciliation Statement [1]

Read the following hypothetical situation, answer question nos. 9 and lo.

The business which follows the convention of prudence keeps provisions and reserves so that they can maintain liquidity of the firm and help it in the time of crisis. But, what are exactly Reserves and Provisions. When we talk about provisions, they mean setting aside a part of the profits for meeting a known future liability, the amount of which is not accurately known at the time of finalization of financial statements.

It is made for meeting known future liability. The amount, of the liability cannot be determined accurately. It is charge against profit thereby reducing the profit. Provisions serve a lot of purposes. It helps in ascertaining the true net profit of the entity. The true financial position can be determined adequately. It helps in providing funds for liabilities that may occur in future. It helps in the proper allocation of expenses that are incurred over time.

Reserves, on means an appropriation of profits or other surplus to strengthen the liquid resources of the business enterprise and not for meeting any liability, contingency or any commitment of the business. They are retained or undistributed net profit. It is voluntarily done to strengthen the financial position of the firm. It can be used for investing in outside securities. Like provisions, reserves are also very important for the business enterprises. It helps in meeting any unforeseen expenses. It strengthens the financial position of the firm. It helps in equal distribution of profit. It helps in providing funds to meet liability.

Answer:

(C) (i), (ii) and (iii)

OR

(A) Pass Book

Explanation: Pass Book is the statement of transactions done with the bank. Cash book records all the cash

transactions. Cheque Book is used to withdraw money from the Bank. Bank Reconciliation Statement is prepared when Cash Book and Pass Book have some discrepancies.

Question 9.

Which of the following is not a characteristic of Provisions:

(A) It is made for meeting known future liability.

(B) The amount of liability cannot be determined accurately.

(C) It is charge against profit thereby reducing the profit.

(D) They are retained or undistributed net profit. [1]

Answer:

(D) They are retained or undistributed net profit.

Question 10.

Which of the following is not an importance of Reserve:

(A) It helps in meeting any unforeseen expenses.

(B) It strengthens the financial position of the firm.

(C) It helps in equal distribution of profit.

(D) It helps in providing funds for the liabilities that may occur in future. [1]

Answer:

(D) It helps in providing funds for the liabilities that may occur in future.

Question 11.

Which concept states that business is separate from its owner?

(A) Going Concern

(B) Accounting Period

(C) Business Entity

(D) Conservatism [1]

Answer:

(C) Business Entity

Explanation: According to this assumption, a business unit should be understood as a separate entity apart from the businessman. Transactions of business should not be merged with the personal transactions of businessman. When the owner invests money into the business it should be assumed that the business owes money to the owner. This is known as capital. Capital is the amount which a business owes to its owner.

Question 12.

Business is a going concern; the owners cannot wait for a long period to know the results of their business as it may not serve the purpose of owners and other interested parties. The users of financial information need periodical reporting relating to the performance of the business. Normally, accounting period is one year. Which Accounting Principle is being discussed?

(A) Going Concern

(B) Accounting Period

(C) Conservatism

(D) Consistency [1]

Answer:

(B) Accounting Period

Question 13.

Rent paid ₹ 1,000. So this transaction has two aspect one is debit as rent and other is cash which will be credit. Under which accounting concept is this done?

(A) Business Entity

(B) Going Concern

(C) Dual Aspect

(D) None of the these [1]

Answer:

(C) Dual Aspect

Explanation: According to Dual Aspect principle every business transaction has two aspects, i.e., debit and credit with same amount.

Question 14.

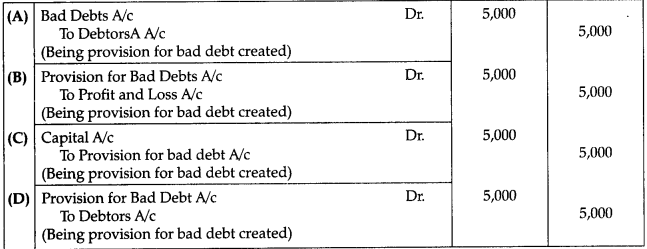

Anu charges 10% provision for bad debts on the debtors, book value being 5O,OO0. Pass the following journal entry?

Answer:

Option (D) is correct.

Question 15.

Consider the following statements with respect to the purpose of maintaining the Subsidiary Books:

(i) It saves time and effort in recording transactions.

(il) It enables division of work leading to an enhancement of efficiency and effectiveness, as particular accountant takes care of particular books.

(iii) It also makes each accountant more responsible and accountable for the books assigned to them.

Identify the correct statement/statements:

(A) (i) and (ii)

(B) (i) only

(C) (i), (ii) and (iii)

(D) (iii) only [1]

OR

Which type of sales are recorded in sales book?

(A) All type of sales

(B) Only credit sales of goods

(C) Credit sale of any item

(D) Cash sale of any item [1]

Answer:

(C) (i), (ii) and (iii)

OR

(B) Only credit sales of goods

Explanation: Credit sales of other items are recorded in journal proper.

Question 16.

Explain the qualitative characteristics of accounting information. [3]

OR

Explain the following Assump6onfPiinciples of Accounting:

(i) Going Concern Assumption

(ii) Consistency Assumption

(iii) Matching Principle. [3]

Answer:

The following are the qualitative characteristics of accounting information :

(i) Reliability : It means that the user can rely on the accounting information. All accounting information is verifiable and can be verified from the source document (voucher), viz. cash memos, bills, etc. Hence, the available information should be free from any errors and bias.

(ii) Relevance : It means that essential and appropriate information should be easily and timely available and any irrelevant information should be avoided. The users of accounting information need relevant information for decision-making, planning and predicting the future conditions.

(iii) Understandability : Accounting information should be presented in such a way that every user is able to interpret the information without any difficulty in a meaningful and appropriate manner.

(iv) Comparability : It is the most important quality of accounting information. Comparability means accounting

information of a current year can be compared with that of the previous years. Comparability enables intra¬firm and inter-firm comparison. This assists in assessing the outcomes of various policies and programmes adopted in different time horizons by the same or different businesses. Further, it helps to ascertain the growth and progress of the business over time and in comparison to other businesses.

OR

The following Assumptions/Principles of Accounting are:

(i) Going Concern Assumption: All the transactions in accounting books are recorded on the basis of the assumption that trade will continue for unlimited period. However, it does not mean that trade is immortal and permanent. In the absence of liquidation, it is assumed that the trade will continue for a long period. The accounts are not affected easily by fear of changes or by dissolution of trade.

(ii) Consistency Assumption: The accounting information provided by the financial statements would be useful in drawing conclusions regarding the working of an enterprise only when it allows comparisons over a period of time as well as with the working of other enterprises. Thus, both inter-firm and inter-period comparisons are required to be made. This can be possible only when accounting policies and practices followed by enterprises are uniform and are consistent over the period of time.

(iii) Matching Principle: The process of ascertaining the amount of profit earned or the loss incurred during a particular period involves deduction of related expenses from the revenue earned during that period. The matching concept emphasizes exactly on this aspect. It states that expenses incurred in an accounting period should be matched with revenues during that period. It follows from this that the revenue and expenses incurred to earn these revenues must belong to the same accounting period.

Question 17.

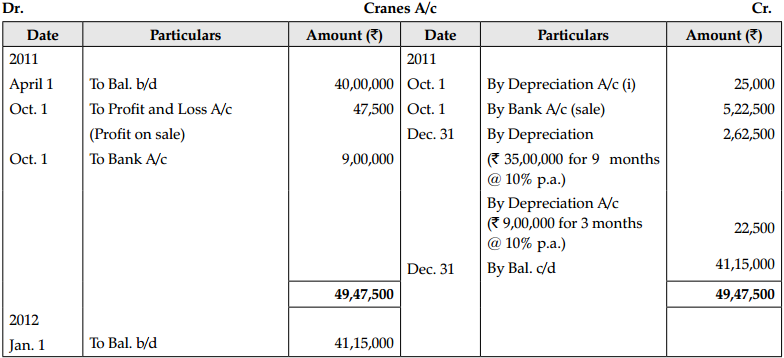

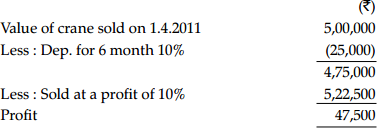

A Noida based Construction Company owns 5 cranes and the value of these assets in its books on April 01, 2011 is ₹ 40,00,000 On October 01, 2011 it sold one of its cranes whose value was ₹ 5,00,000 on April 01, 2011 at a 10% profit. On the same day it purchased 2 cranes for ₹ 4,50,000 each. Prepare Cranes Account. It closes the books on December 31 and provides for depreciation on 10% written down value. [3]

Answer:

Working notes

Question 18.

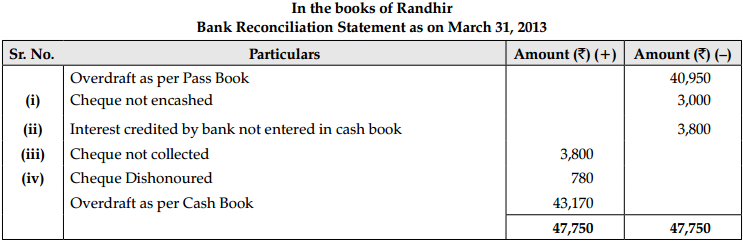

The pass book of Mt Randhir showed an overdraft of ₹ 40,950 on March, 31 2013. Prepare Bank Reconciliation Statement on March 31, 2013.

(i) Out of cheques amounting to ₹ 8,000 drawn by Mr. Randhir on March 27, a cheque for ₹ 3,000 was encashed on April 2014.

(ii) Credited bank with ₹ 3,800 for interest collected by them, but the amount is not entered in the cash book.

(iii) ₹ 10,900 paid in by Mr. Randhir in cash and by cheques on March, 31 cheques amounting to ₹ 3,800 were collected on April, 07.

(iv) A cheque of ₹ 780 credited in ti ie pass book on March 28 being dishonoured debited again in the pass book ón

April 01,2014. There was no entry in the cash book about the dishonour of the cheque until April 15. [3]

Answer:

Question 19.

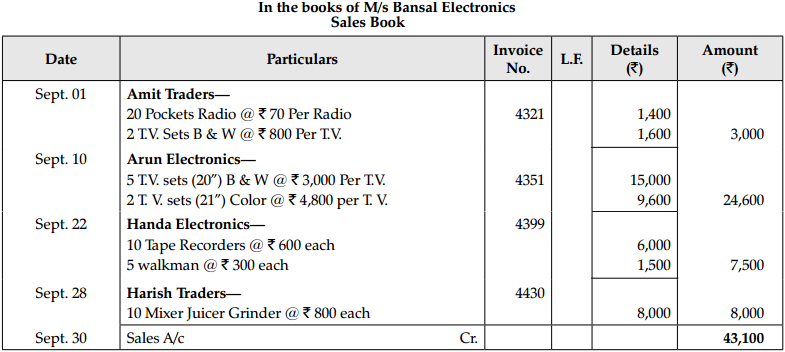

Enter the following transactions in Sales Journal (Book) of M/s Bansal Electronics:

| 2014 | |

| September | |

| 01 | Sold to Amit Traders as per Bill No. 4321 |

| 20 Pocket Radio @ ₹ 70 per Radio | |

| 2 TV Set, B & W, (6”) @ ₹ 800 per TV | |

| 10 | Sold to Arun Electronics as per Bill no. 4351 |

| 5 TV Set (20”) B & W @ ₹ 3,000 Per TV | |

| 2 TV Sets (21”) Colour @ ₹ 4,800 Per TV | |

| 22 | Sold to Handa Electronics as per Bill No. 4,399 |

| 10 Tape recorders : ₹ 600 Each | |

| 5 Walkman @ ₹ 300 Each | |

| 28 | Sold to Harish Traders as per Bill No. 4,430 |

| 10 Mixer juicer Grinder @ ₹ 800 Each. |

Answer:

Question 20.

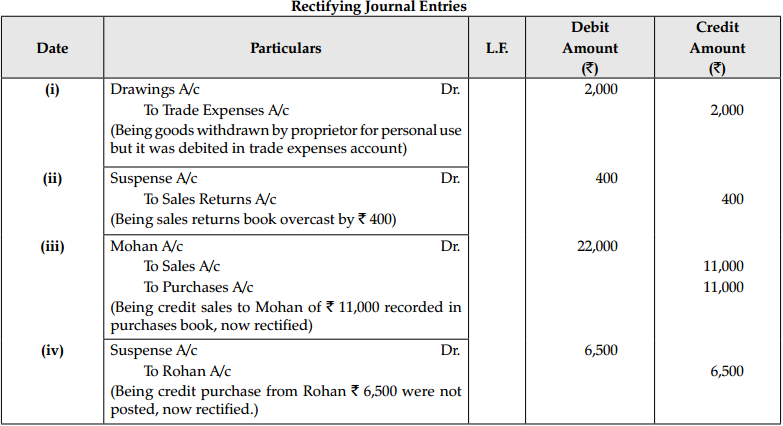

Rectify the following errors:

(i) Goods withdrawn by proprietor for personal use 2,000 were debited to trade expenses account.

(ii) Sales returns book overcast by 400.

(iii) Credit sales to Mohan 11,000 were recorded in purchases book.

(iv) Credit purchases from Rohan 6,500 were not posted to his account. [4]

Answer:

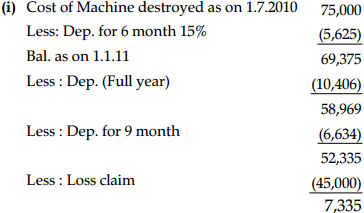

Question 21.

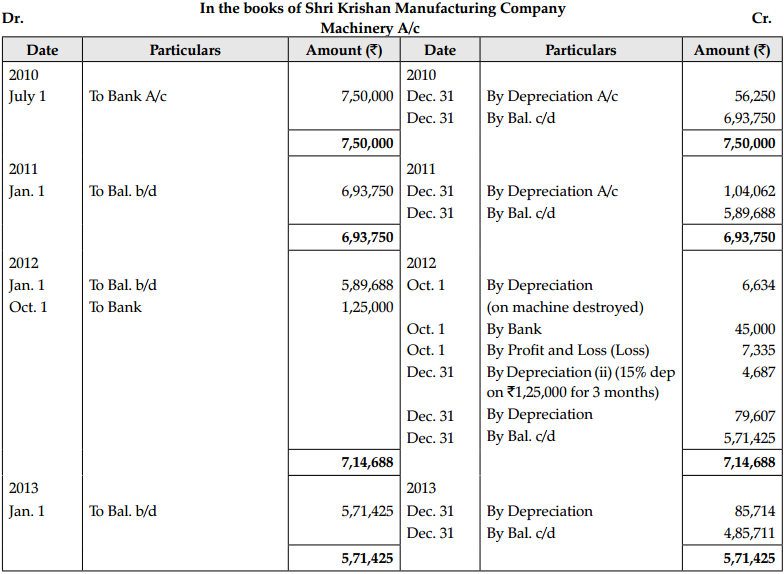

Shri Krishan Manufacturing Company purchased 10 machines at ₹ 75,000 each on July 01, 2010. On October 01, 2012, one of the machines got destroyed by fire and an Insurance claim of 45,000 was admitted by the company. On the same date another machine is purchased by company for ₹ 1,25,000. The company writes off 15 % p.a. depreciation on written down value basis. The company maintains the calendar year as its financial year.

Prepare the machinery account from 2010 to 2013. [6]

OR

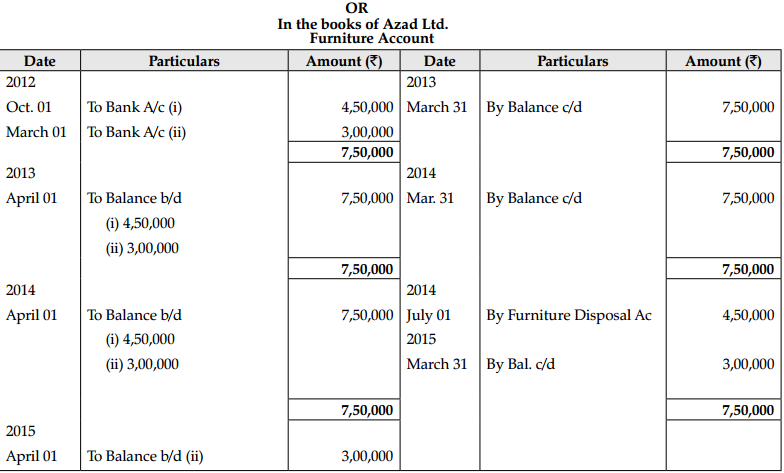

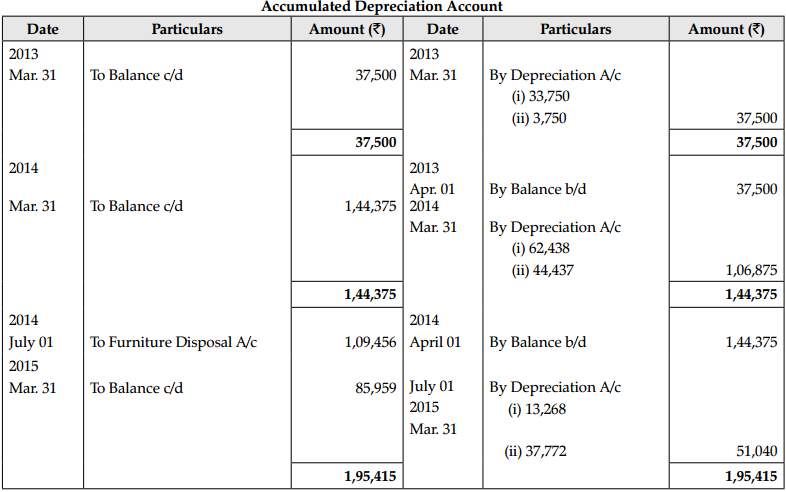

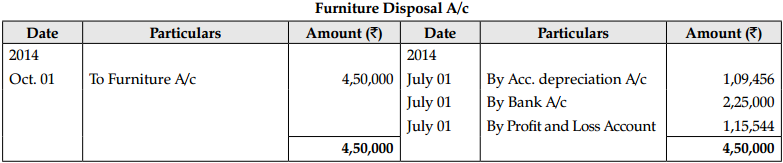

Azad Ltd. purchased furniture on October 01,2012 for ₹ 4,50,000. On March 01,2013 it purchased another furniture for ₹ 3,00,000. On July 01, 2014 it sold off the first furniture purchased in 2012 for ₹ 2,25,000. Depreciation is provided at 15% p.a. on written down value method. Prepare Furniture account, and Accumulated depreciation account for the years ended on March 31, 2003, March 31, 2014 and March 31, 2015. Also, give the above two accounts if furniture Disposal Account is opened. [6]

Answer:

Working notes

(ii) Depreciation on Machines purchased

(15% depreciation on ₹ 1,25,000 for 3 months) = 4,687

OR

Question 22.

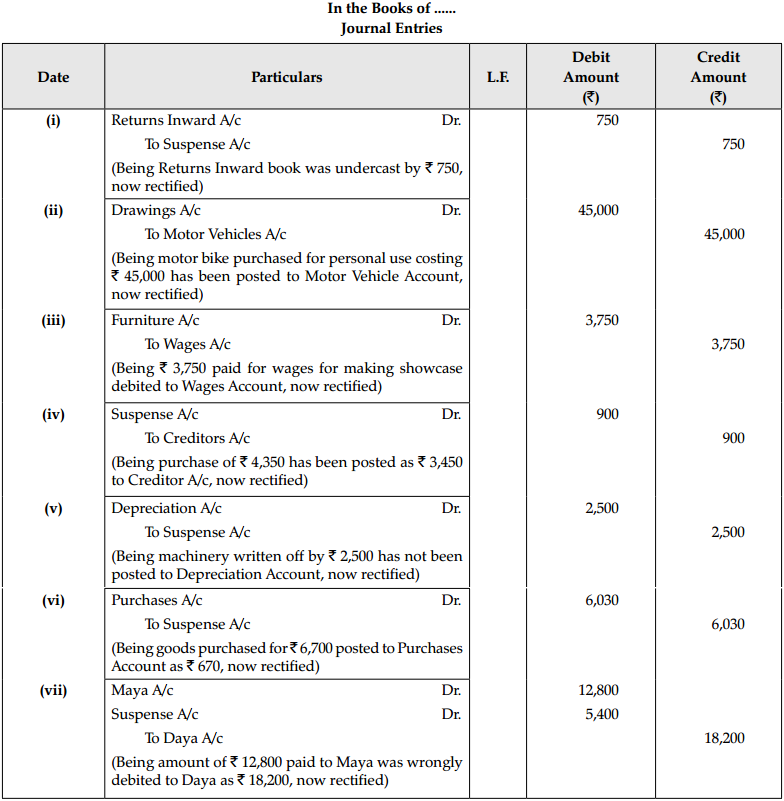

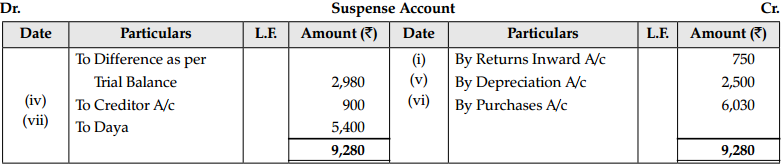

Thé TI-ial Balance of Mr. Rameshwar had 2,980 excess credit. The difference has been posted to Suspense Account. Subsequently, the following erros were discovered. You are required to pass necessary entries for rectifying the errors and also show the Suspense Account:

(i) Total of Returns Inward Book was cast by 750 short.

(ii) Purchase of Motor bike for personal use costing 45,000 had been posted to Motor Vehicle A/c.

(iii) An amount of ?3,750 paid for wages for making show cases had been charged to Wages A/c.

(iv) Purchase of ‘4,350 has been posted to Creditors Account as 3,450.

(v) Machinery was written off by 2,500 has not been posted to Depreciation A/c.

(vi) Goods purchased for 6,700 were posted as 670 to purchases Nc.

(vii) Amount of 12$00 paid to Maya was wrongly debited to Daya as 18,200. [6]

OR

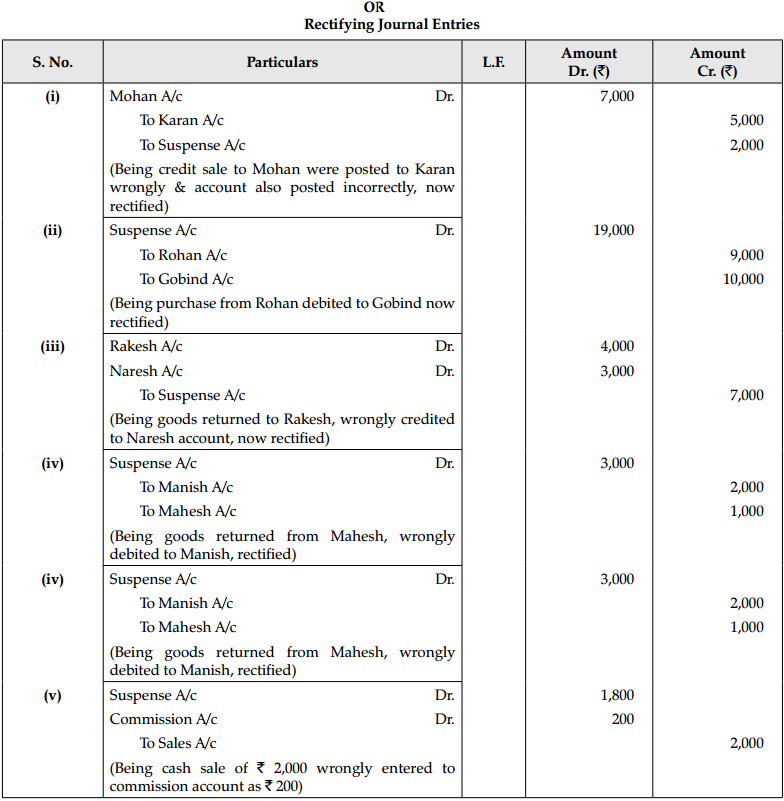

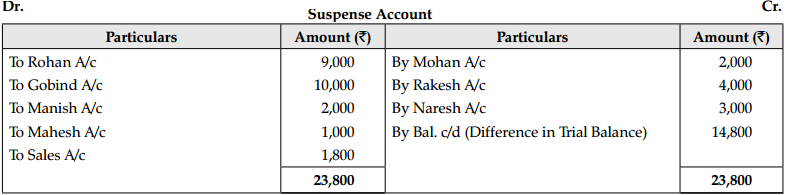

Rectify the following errors assuming that a suspense account was opened. Ascertain the difference in trial balance.

(j) Credit sales to Mohan Z 7,000 were posted to Karan as 5,000.

(ii) Credit purchases from Rohan Z 9,000 were posted to the debit of Gobind as 10,000.

(ili) Good returned to Rakesh Z 4,000 were posted to the credit of Naresh as Z 3,000.

(iv) Goods retrned from Mahesh Z 1,000 were posted to the debit of Manish as Z 2,000.

(v) Cash sales Z 2,000 were posted to Commission account as Z 200. [6J

Answer:

Question 23.

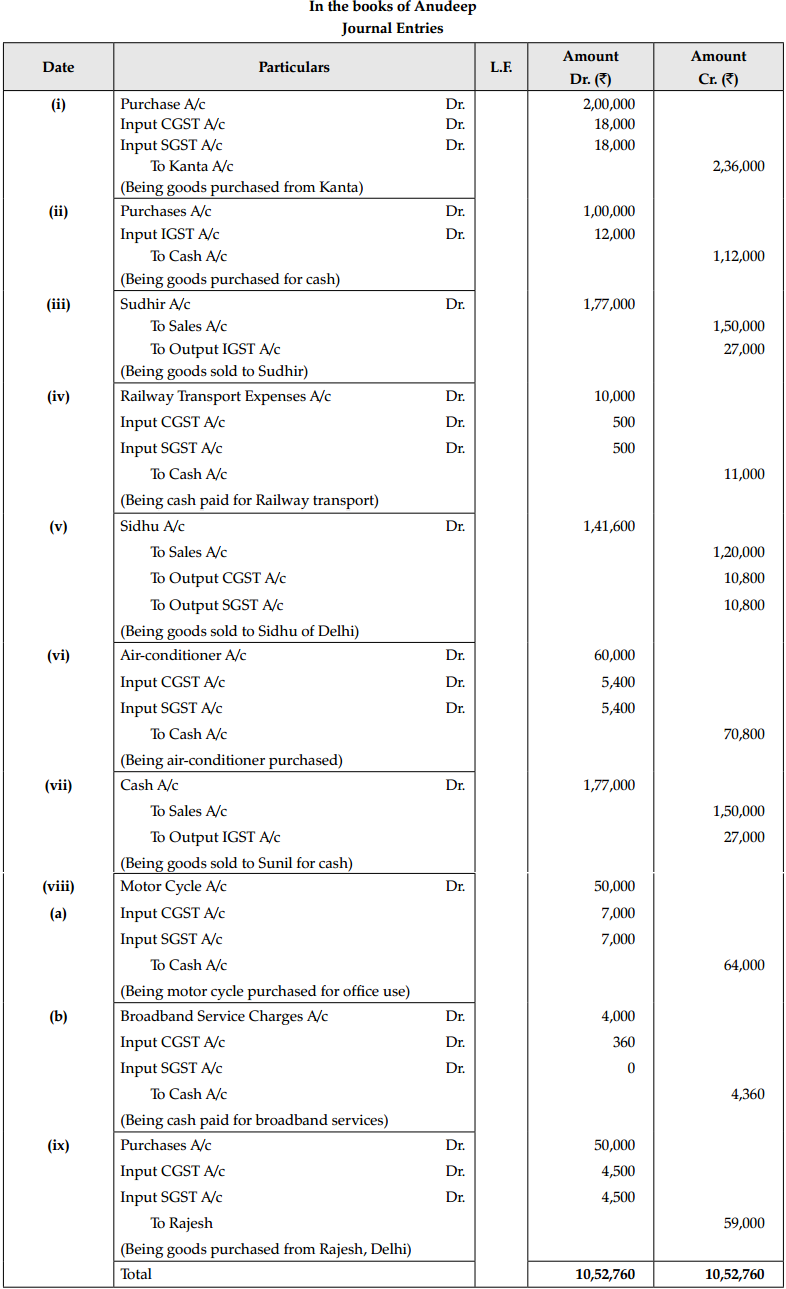

Record journal entries for the following transactions in the books of Anudeep of Delhi:

(i) Bought good Z 2,00,000 from Kanta of Delhi (CGST @ 9%, SGST @9%)

(ii) Bought good Z 1,00,000 for cash from Rajasthan (IGST @ 12%)

(iii) Soki goods Z 1,50,000 to Sudhir of Punjab (IGST @ 18%)

(iv) Paid for Railway Transport Z 10,000 (CGST @ 5%, SGST @ 5%)

(v) Sold goods Z 1,20,000 to Sidhu of Delhi (CGST @9%, SGST @9%)

(vi) Bought Air-condition for office use Z 60,000 (CGST @9%, SGST @9%)

(vii) Sold goods 1,50,000 for cash to Sunil of Uttar Pradesh (IGST 18%)

(viii)Bought Motor Cycle for business use Z 50,000 (CGST @ 14%, SGST @ 14%). Paid for broadband services Z 4,000 (CGST @9%, SGST @0%)

(ix) Bought good Z 50,000 from Rajesh, Delhi (CGST @ 9% SGST @9%) [6]

Answer:

Question 24.

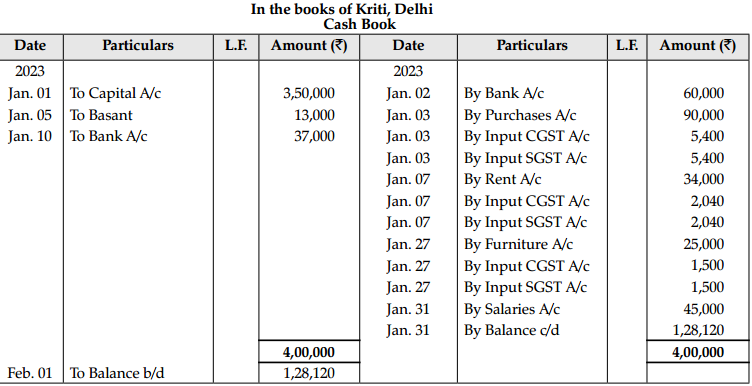

Enter the following transactions in a simple Cash Book of Kriti, Delhi:

| 2023 | Particulars | ₹ |

| Jan. 01 | Started Business with Cash | 3,50,000 |

| Jan. 02 | Opened a bank account and deposited | 60,000 |

| Jan. 03 | Purchased goods for cash for 90,000 plus CGST and | |

| SGST « 6% each from Anup Electricals, Delhi | ||

| Jan. 03 | Sold goods of 45000 plus IGST @ 12% to | |

| Bhavesh of Chandigarh on credit. | ||

| Jan.05 | Received from Basant | 13,000 |

| Jan.07 | Paid Rent of 34000 pIus CGST and SGST @ 6% each | |

| Jan. 10 | Withdrew cash from bank | 37,000 |

| Jan. 27 | Purchased furniture in Cash ? 25,000 plus CGST | |

| and SGST @ 6% each from a trader of Delhi | ||

| Jan.31 | Paid Salaries | 45,000 |

Answer:

Part-B (Financial Accounting – II)

Question 25.

“Full amount of loss is shown in the credit side of Trading Account and is also shown in the assets side of Balance sheet.” For which item is this adjustment related to?

(A) Abnormal loss in the uninsured stock

(B) Abnormal loss in the insured stock

(C) Both (A) and (B)

(D) Neither (A) nor (B) [1]

OR

X is confused regarding the adjustment of interest on drawings in the balance sheet. Help him to transact it.

(A) Deducted from drawings

(B) Deducted from loan

(C) Deducted from capital

(D) Deducted from creditors [1]

Answer:

(B) Abnormal loss in the insured stock

OR

(C) Deducted from capital

Explanation: Interest on drawings is treated as drawings and so will be a charge on the capital of the firm.

Question 26.

Which one item of the following is shown as a deduction from purchases in Trading Account:

(A) Goods taken for personal use of proprietor

(B) Goods distributed as free sample

(C) Abnormal loss of stock

(D) All of the above [1]

Answer:

(D) All of the above

Explanation: Any transaction that involves the loss of goods or giving of goods for charity or for free or as a promotion, that is the good has not been sold yet but the stock is decreasing, it is to be charged against purchases.

Question 27.

Statement I: Expenses paid in advance are called prepaid expenses.

Statement II: Prepaid or unexpired expenses are deducted from respective item of expenses on the debit side of the Trading and Profit & Loss Account and will appear on the assets side of Balance Sheet as a separate item.

(A) Both Statements are correct.

(B) Both Statements are incorrect.

(C) Statement I is correct and Statement His incorrect.

(D) Statement I is incorrect and Statement Ills correct. [1]

OR

How is goods sold on approval basis adjusted in the final accounts?

(A) Sales amount is deducted from sales in Trading A/c

(B) Sales amount is deducted from debtors in the Balance Sheet.

(C) Cost of such goods is added to closing stock shown on the credit side of the Trading A/c.

(D) All of the above. [1]

Answer:

(A) Both Statements are correct.

OR

(D) All of the above.

Question 28.

Which of the system is considered as authentic by the Court?

(A) Single Entry System

(B) Accounting for incomplete records

(C) Double Entry System

(D) All of the above Lii

Answer:

(C) Double Entry System

Question 29.

Accounts maintained based on this system are not accepted by sales-tax and income-tax authorities. Which system are we talking about?

(A) Incomplete Records

(B) Single Entry System

(C) Both (A) and (B)

(D) None of the above [iJ

Answer:

(C) Both (A) and (B)

Question 30.

Opening Stock 50,000 Purchases 58,200, Expenses on purchases 42,000 Sales 1,70.000, Expenses on sales 41,000 Closing Stock 52,200. Calculate Cost of Goods Sold and Gross Profit. [3]

OR

Drawings 75,000, Profit for the year 95,000, Closing Capital 2,98,000. Calculate the Opening Capital. Also explain

the meaning of capital. [3]

Answer:

Cost of Goods Sold = Opening stock + Purchases + Expenses on purchases – Closing Stock

= ₹ 50,000 + ₹ 58,200 + ₹ 42,000 – ₹ 52,200 = ₹ 98,000

Gross Profit = Net Sales – Cost of goods sold

= ₹ 1,29,000 – ₹ 98,000 = ₹ 31,000 [3]

OR

Profit = Closing Capital + Drawings – Additional Capital – Opening Capital.

₹ 95,000 = ₹ 2,98,000 + ₹ 75,000 – 0 – Opening Capital.

Opening Capital = ₹ 3,73,000 – ₹ 95,000 = ₹ 2,78,000 [3]

Capital is the amount invested by the owner in his firm. This investment can be in the form of cash or goods. The net profit of the firm helps in increasing the owners’ capital whereas a net loss decreases it as these are added/ deducted respectively from the capital.

Question 31.

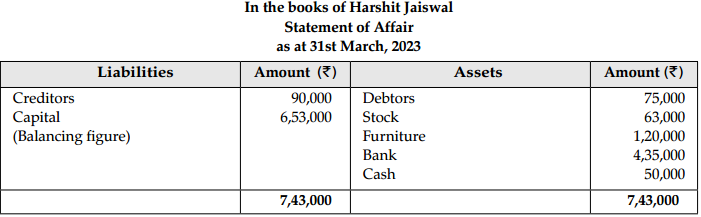

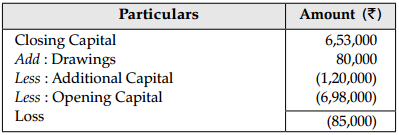

Harshit Jaiswal started a business with a capital of ₹ 6,98,000 and maintains his account on Single Entry System. Calculate his profit on 31st March, 2023 from the following information:

| Liabilities and Assets as at 31st March, 2023 | ₹ |

| Debtors | 75,000 |

| Creditors | 90,000 |

| Stock | 63,000 |

| Furniture | 1,20,000 |

| Bank Balance | 4,35,000 |

| Cash-in-hand | 50,000 |

During the year his drawings were ₹ 80,000 and additional capital invested ₹ 1,20,000.

Answer:

Calculation of Profit :

Question 32.

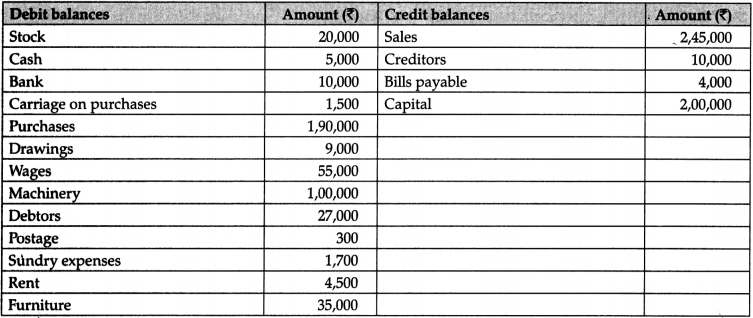

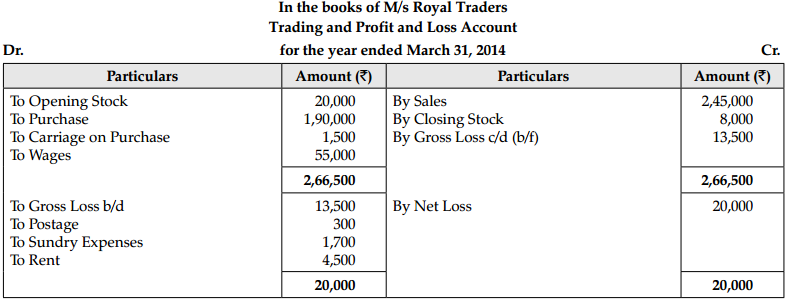

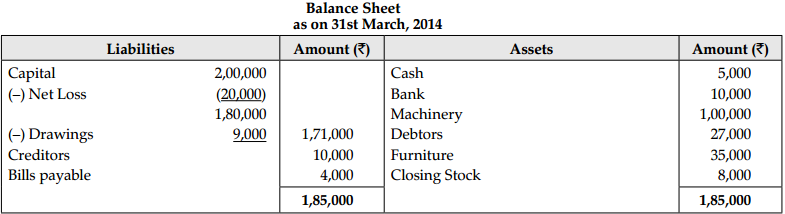

Prepare Trading and Profit and Loss Account and Balance Sheet of M/s Royal Traders from the following balances as on March 31, 2014.

Closing stock ₹ 8,000. [3]

Answer:

Question 33.

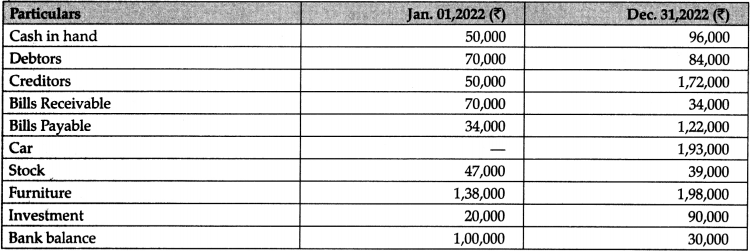

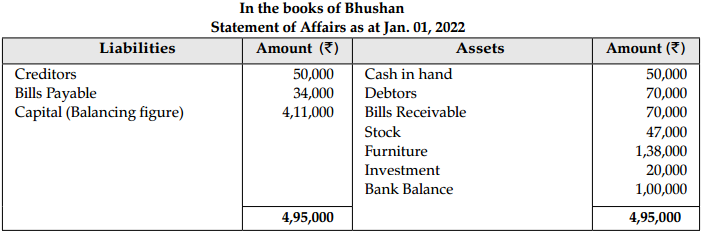

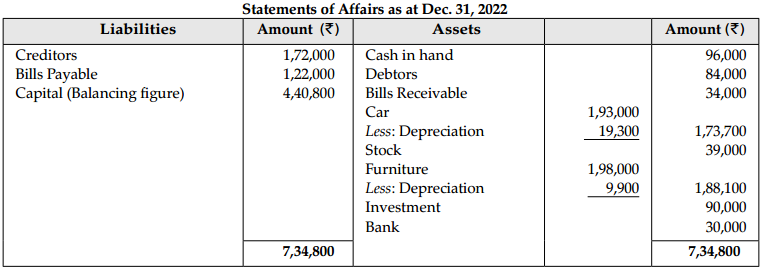

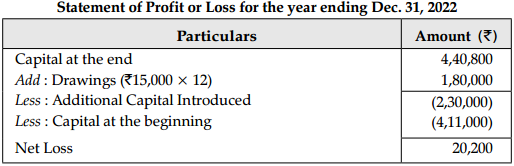

Bhushan Gandhi has not kept proper books of accounts, prepare the statement of profit or loss for the year ending December 31, 2022 from the following information:

The following adjustments were made:

(I) Bhushan withdrew cash ₹ 15,000 per month for private use.

(il) Depreciation @ 10% on car and furniture @ 5%

(iii) Fresh Capital introduced during the year ₹ 2,30,000. [4]

OR

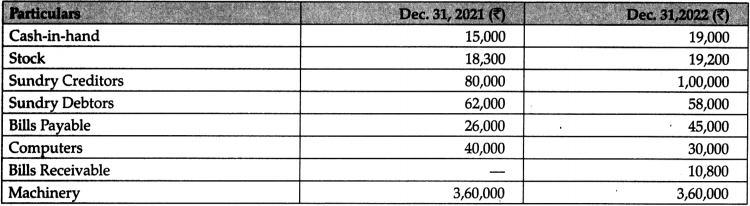

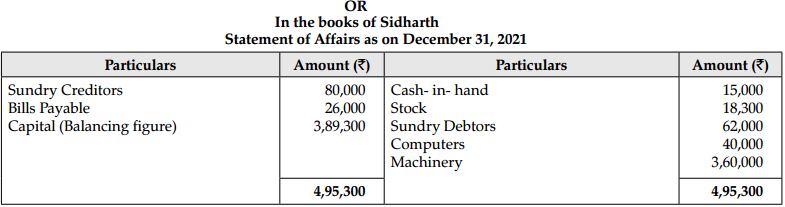

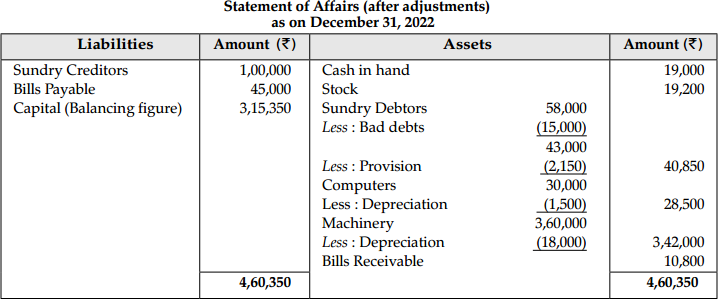

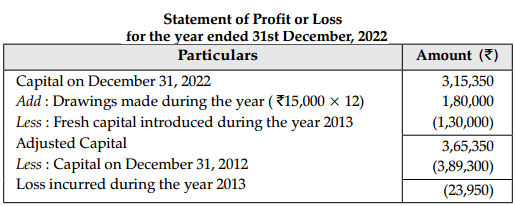

Sidharth does not keep proper records. From the following information find out profit or loss and also prepare Statement of Affairs for the year ended December 31, 2022.

Shyam informs about his transactions: Drawings 15,000 p.m. for personal use, fresh capital introduce during the year 1,30,000.

Computers and Machinery are to be depreciated @ 5% p.a. A provision of 5% is to be made on debtors for doubtful debts. It was found that 15,000 is irrecoverable from debtors. [4]

Answer:

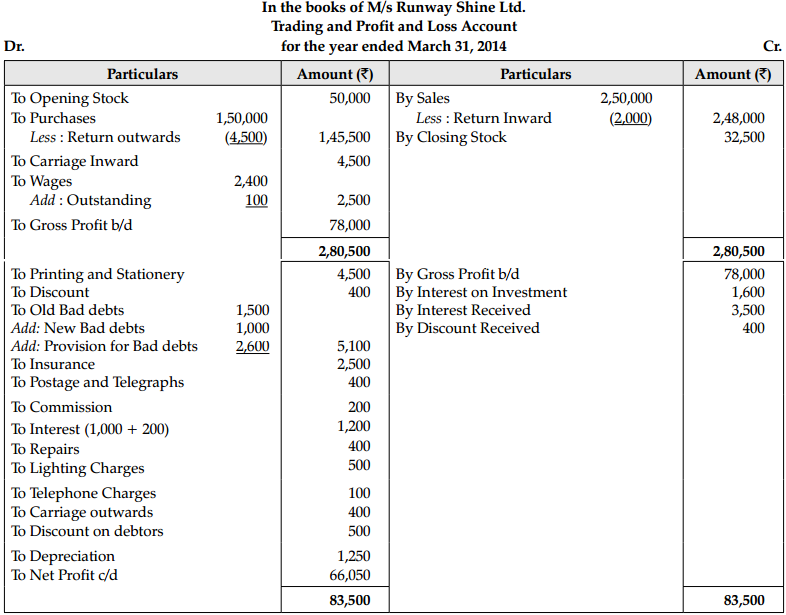

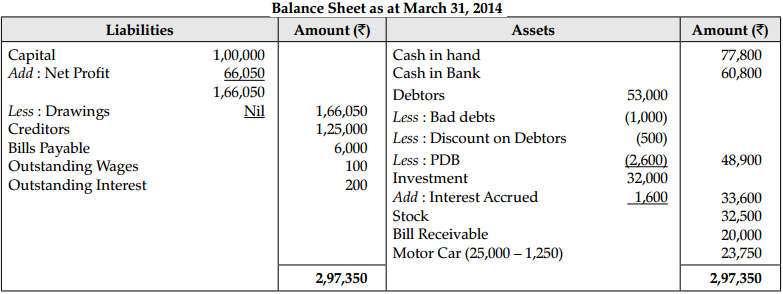

Question 34.

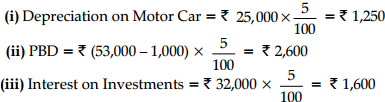

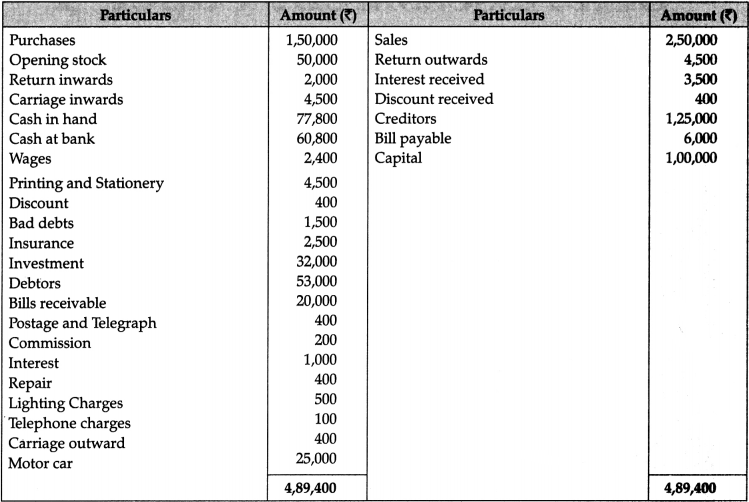

The following balances have been extracted from the trial balance of M/s Runway Shine Ltd. Prepare a trading and Profit and Loss Account and a Balance Sheet as on March 31, 2014.

Adjustments:

(j) Further bad debts 1,000. Discount on debtors 500 and make a provision on debtors @ 5%.

(li) Interest to be received on investment @ 5%.

(iii) Wages and interest outstanding 100 and 200 respectively.

(iv) Depreciation charged on motor car @ 5% p.a.

(v) Closing Stock 32,500.

Answer:

Working Notes: