Students can access the CBSE Sample Papers for Class 11 Accountancy with Solutions and marking scheme Set 1 will help students in understanding the difficulty level of the exam.

CBSE Sample Papers for Class 11 Accountancy Set 1 with Solutions

Time Allowed : 3 hours

Maximum Marks: 70

General Instructions:

- This question paper contains 34 questions. All questions are compulsory.

- This question paper is divided into two parts, Part A and B.

- Question Nos. 1 to 15 and 25 to 29 carries 1 mark each.

- Questions Nos. 16 to 18,30 to 32 carries 3 marks each.

- Questions Nos. 19,20 and 33 carries 4 marks each

- Questions Nos. from 21 to 24 and 34 carries 6 marks each

- There is no overall choice. However, an internal choice has been provided in 7 questions of one mark, 2 questions of three marks, 1 question of four marks and 2 questions of six marks

Part – A ((Financial Accounting – I)

Question 1.

Which of the following can be converted into cash within a very short period of time:

(A) Fixed Assets

(B) Current Assets

(C) Liquid Assets

(D) Intangible Assets [1]

Answer:

(C) Liquid Assets

Explanation: Liquid assets are the assets which can be converted to cash easily. For example Cash at bank.

Question 2.

‘Assertion: Contingent Liabilities are not actually liabilities.

Reason: They are probable liabilities which are dependent on the happening of a certain contingency.

(A) Both A and R are correct, and R is the correct explanation of A.

(B) Both A and R are correct, but R is not the correct explanation of A.

(C) A is correct, but R is incorrect.

(D) A is incorrect, but R is correct. [1]

Answer:

(A) Both A and R are correct, and R is the correct explanation of A.

Question 3.

Consider the following statements with regard to the advantages of Accounting:

(i) ‘Easy availability of information.

(ii) Financial accounting shows the exact worth of business.

(iii) It identifies strength and weaknesses of the business.

(iv) It enables comparison between two different periods and between similar companies.

Identify the correct statement/statements:

“Accounting data does not reflect the true and fair view of the affairs of an enterprise.” To which accounting principle does this limitation relate?

(A) Dual Aspect

(B) Materiality

(C) Money Measurement

(D) Going Concern [1]

OR

Current liabilities are the liabilities which are payable within …………….

(A) Six months

(B) One year

(C) Two years

(D) Three months [1]

Answer:

(C) Money Measurement

OR

(B) One year

Question 4.

Which of the following is not a fundamental accounting assumption:

(A) Going concern

(B) Accrual

(C) Consistency

(D) Verifiable Objective Evidence [1]

OR

“Accounting data does not reflect the true and fair view of the affairs of an enterprise.” To which accounting principle does this limitation relate?

(A) Dual Aspect

(B) Materiality

(C) Money Measurement

(D) Going Concern [1]

Answer:

(D) Verifiable Objective Evidence

Explanation: Verifiable objective evidence is not a fundamental accounting assumption. This principle justifies the significance of verifiable documents supporting various transactions.

OR

(C) Money Measurement

Explanation: Money measurement concept restricts the scope of accounting to factors that are measurable in terms of money. It says only the transactions measurable in terms of money are to be recorded. While we can record values of various assets and liabilities, we cannot record the level of satisfaction of our customers and loyalty of our employees. We can say our customers are ‘happy’ or ‘very happy’, but we cannot write in our accounts how much our customers are happy, simply because ‘happiness’ cannot be measured in terms of money.

Question 5.

An advantage of assumption is that financial statements become comparable and meaningful.

(A) Consistency

(B) Matching Cost

(C) Accounting Period

(D) Going Concern [1]

Answer:

(A) Consistency

Explanation: The accounting information provided by the financial statements would be useful in drawing conclusions regarding the working of an enterprise only when it allows comparisons over a period of time as well as with the working of other enterprises. Thus, both inter-firm and inter-period comparisons are required to be made. This can be possible only when accounting policies and practices followed by enterprises are uniform and are consistent over the period of time.

Question 6.

For which of the following transaction, journal proper will not be used:

(A) Purchased fixed asset for cash

(B) Purchased fixed asset on credit

(C) Depreciation charged

(D) Outstanding expenses [1]

OR

Cash book does not record transaction of:

(A) Cash nature

(B) Credit nature

(C) Cash and credit nature

(D) None of these [1]

Answer:

(A) Purchased fixed asset for cash

Explanation: Cash transactions are recorded in the Cash Book. Journal Proper records all the credit transactions.

OR

(B) Credit nature

Question 7.

Assertion: Maintenance of subsidiary books allows specialisation of accounts.

Reason: Various accounting entries can be undertaken simultaneously because of the use of number of books.

(A) Both A and R are correct, and R is the correct explanation of A.

(B) Both A and R are correct, but R is not the correct explanation of A.

(C) A is correct, but R is incorrect.

(D) A is incorrect, but R is correct.

Answer:

(B) Both A and R are correct, but R is not the correct explanation of A.

Question 8.

According to which concept, all expenses incurred to earn revenue of a particular period should be charged against that revenue to determine the net income?

(A) Conservatism

(B) Business entity

(C) Accounting period

(D) Matching [1]

OR

Financial Statements of an entity are prepared at regular intervals in accordance to which accounting concept?

(A) Conservatism

(B) Business entity

(C) Accounting period

(D) Matching [1]

Read the following hypothetical situation, answer question nos. 9 and 10.

On the 1st of May 2018, Shri Enterprises had a cash balance of ₹ 12,400 and a bank balance of ₹ 36,000. Mr. Ganesh, one of the debtors deposited a cheque worth ₹ 10,000 on the 3rd of May and on 5th May Mr. Suresh was paid via cheque of ₹ 7,700 for the full settlement of the account of ₹ 8,000. The cheque received on the 6th worth ₹ 12,000 from Mr. Xavier was deposited on the 7th of May. On the 8th ₹ 22,000 was received in cash and ₹ 8,000 was deposited in the bank. The cheque given by Mr. Xavier was dishonoured and for which ₹ 20 was paid as bank charges. On the 20th of May, a bill receivable was discounted worth ₹ 10,000 at 1% through the bank. On the 26th the proprietor withdrew ₹ 10,000 from the bank from which he used ₹ 8,000 for office use.

Answer:

(D) Matching

Explanation: Matching principle suggests that we must match the revenue of a particular period with expenses of that particular period only to get correct profits. Business is carried out with the intention of making profits. Profit is the excess of revenue over expenditure. It is the net increase in assets due to business activity. To ascertain the profit for a period, a businessman must identify the revenue for a period, and compare it with the expenses related to earn that revenue. When his revenue is more than the expenditure, he has earned profit. This requires adjustments of certain items like prepaid and outstanding expenses, accrued and advance income.

OR

(C) Accounting period

Explanation: As per the going concern assumption the life of the business is indefinite. To assess the performance of a business, it is illogical to wait for the life of the business to come to an end and then calculate the profit or loss. To overcome this problem and for the purpose of calculation of profits, the life of the business is divided in smaller parts called ‘accounting period’. An Accounting period is a segment of one year in the indefinite life of a business.

Question 9.

In which account will the cheque deposited by Mr. Ganesh be recorded?

(A) Bank

(B) Cash

(C) Debtors

(D) Both (A) and (C) [1]

Answer:

(D) Both (A) and (C)

Explanation: Every transaction affects two accounts. As Mr. Ganesh, a debtor is paying through cheque, so the bank account will be debited and debtor’s account will be credited.

Question 10.

The amount recorded as drawings will be .

(A) ₹ 2,000

(B) ₹ 8,000

(C) ₹ 10,000

(D) Nil [1]

Answer:

(A) ₹ 2,000

Explanation: ‘10,000 – ‘8,000 = ‘2,000

Question 11.

Which system of accounting is popularly used now-a-days?

(A) Cash basis

(B) Accrual Basis

(C) Single Entry system

(D) Double Entry system [1]

Answer:

(D) Double Entry system

Question 12.

The realisation concept determines when goods sent on credit to customers are to be included in the sales figure for the purpose of computing the profit or loss for accounting period. Which of the following tends to be used in practice to determine when to include a transaction in the sales figure for the period, i.e., when the goods have .been .

(A) Dispatched

(B) Invoiced

(C) Delivered

(D) Paid for [1]

Answer:

(B) Invoiced

Explanation: According to the realisation concept, revenue is recognised when an obligation to receive the amount arises. When the goods are invoiced, it is treated as the transfer of ownership of goods from the seller to the buyer and hence the revenue is recognised.

Question 13.

If a firm believes that some of its debtors may’default’, it should act on this by making sure that all possible losses

are recorded in the books. This is an example of concept.

(A) Conservatism

(B) Accounting entity

(C) Matching

(D) Consistency [1]

Answer:

(A) Conservatism

Question 14.

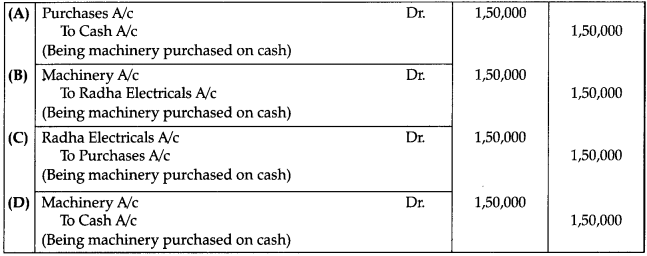

Bikash purchased a machinery for cash from Radha Electricals, which of the following entries will be passed:

Answer:

Option (D) is correct.

Question 15.

Consider the following statements:

Statement I: Pass book is the statement of account of the customer maintained by the bank.

Statement II: A business firm periodically prepares a bank reconciliation statement to reconcile the bank balance as per the cash book with the passbook as these two show different balances for various reasons.

Choose the correct alternatives:

(A) Statement I is true but Statement II is false

(B) Statement I is false but Statement II is true

(C) Both the statements are true

(D) Both the statements are false [1]

OR

Consider the following statements with respect to the features of depreciation:

(i) Depreciation is permanent decline in the value of fixed assets.

(ii) Depreciation is a gradual and continuing process.

(iii) Depreciation is charged on tangible as well as intangible asset.

Identify the correct statement/statements:

(A) (i) and (ii)

(B) (ii) and (iii)

(C) (i) and (iii)

(D) (i) only [1]

Answer:

(C) Both the statements are true

OR

(A) (i) and (ii)

Explanation: Statement (iii) is incorrect as depreciation being decrease in the value of physical assets through normal wear and tear, can only be charged on tangible fixed assets. Intangible assets are amortized.

Question 16.

Explain the characteristics (features) of accounting. [3]

Answer:

Following are the characteristics of accounting :

(i) Economic events : Accounting requires events to be expressed in terms of money. Transactions should involve transfer or exchange of monetary value between the business entity and outsiders.

(ii) Identification, measurement, recording and communication : Accounting is a process of identifying the transactions to be recorded, quantifying the transactions into financial terms, recording the transactions in a systematic manner and communicating the desired information to various interested groups.

(iii) Users of information : Accounting is complete when information is communicated to various groups interested in the functioning of business entity.

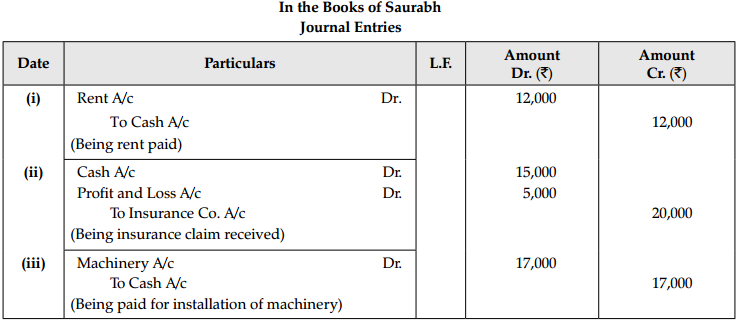

Question 17.

Journalise the following transactions in the books of Saurabh :

(i) Paid ₹ 12,000 for rent.

(ii) Received ₹ 15,000 from insurance company against a claim ₹ 20,000 for loss by fire.

(iii) Paid for installation of machinery ₹ 17,000.

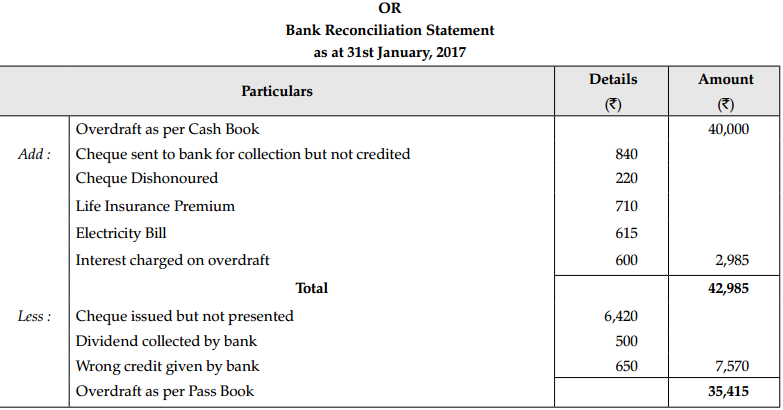

OR

On 31st January, 2017 Cash Book showed an overdraft balance of 40,000. On comparing it with the Pass Book,the

following differences were noticed:

(i) On 27th January, cheques amounting ₹ 6,450 were sent to bank, but out of these one cheque of 840 was

credited on 2nd February and one cheque of ₹ 220 was returned by bank as dishonoured on 31st January.

(ii) During the month of January, cheques were issued worth ₹ 7,580. Out of these, cheques worth ₹ 6,420 were

presented for payment on 5th February.

(iii) As per standing order, the Bank had paid the following amounts during January 2017:

(a) Life Insurance Premium ₹ 710.

(b) Electricity Bill ₹ 615.

(iv) Bank collected ₹ 500 as dividend on shares and gave wrong credit for ₹ 650.

(v) Interest charged on overdraft by the Bank ₹ 600.

Prepare a Bank Reconciliation Statement on 31st January, 2017. [3]

Answer:

Question 18.

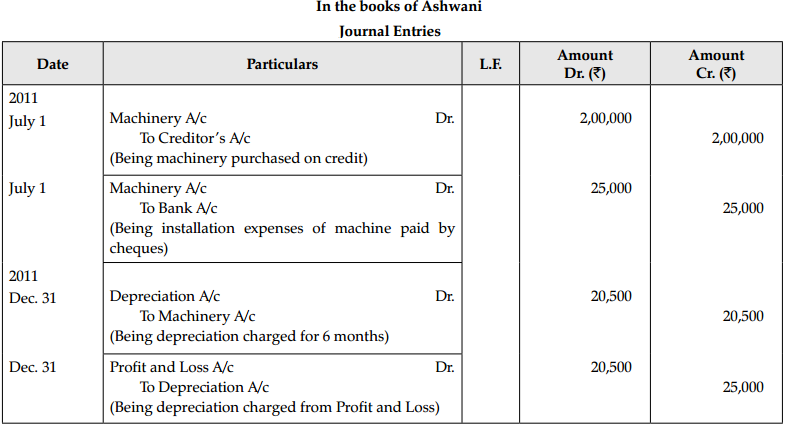

On July 01, 2011 Ashwani purchased a machine for ₹ 2,00,000 on credit. installation expenses ₹ 25,000 are paid by

cheque. The estimated life is 5 years and its scrap value after 5 year will be ₹ 20,000. Depreciation is to be charged

on straight line basis. Show the journal entry for the year 2011. [3]

Answer:

Question 19.

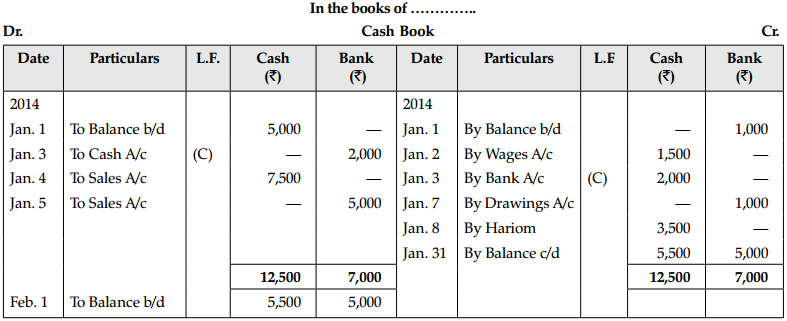

Prepare a Cash Book with Cash and Bank Columns:

| 2014 | Particulars | ₹ |

| Jan. 1 | Cash in Hand | 5,000 |

| Bank Overdraft | 1,000 | |

| Jan. 2 | Paid Wages | 1,500 |

| Jan. 3 | Deposited into bank | 2,000 |

| Jan. 4 | Cash Sales | 7,500 |

| Jan. 5 | Sold goods for cheque which was deposited in bank on the same day | 5,000 |

| Jan. 6 | Purchased goods from Hariom on credit | 4,000 |

| Jan. 7 | Drew from bank for personal use | 1,000 |

| Jan. 8 | Paid to Hariom in full settlement | 3,500 |

Answer:

Question 20.

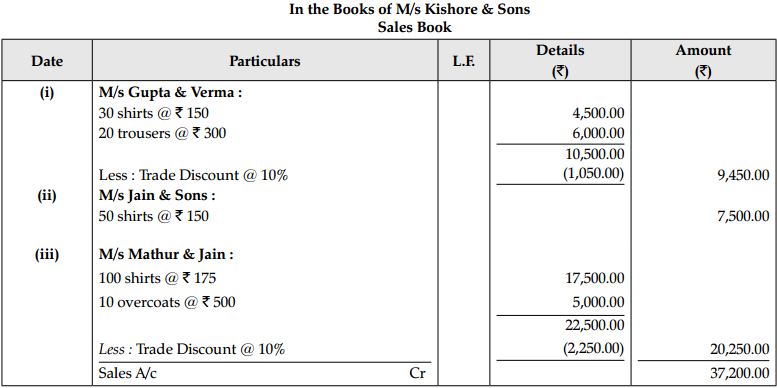

The following are some of the transactions of M/s Kishore & Sons as per Waste Book. Make out their Sales Book:

(i) Sold to M/s Gupta & Verma on credit:

30 shirts @ ₹ 150

20 trousers @ ₹ 300

Less : Trade Discount @ 10%.

(ii) Sold old furniture to M/s Sehgal & Co. on credit ₹ 800

(iii) Sold 50 shirts on credit to M/s Jain & Sons @ ₹ 150 each

(iv) Sold on credit to M/s Mathur & Jain

100 shirts @ ₹ 175

10 overcoats @ ₹ 500

Less : Trade Discount @ 10%. [4]

Answer:

Question 21.

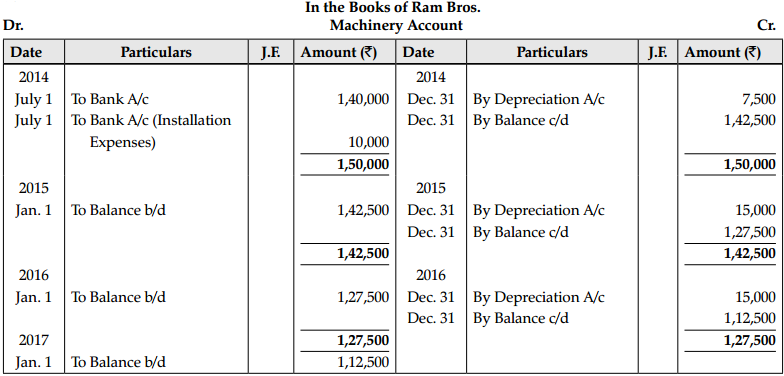

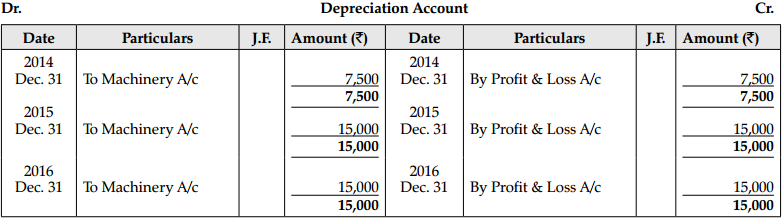

Ram Bros, acquired a machine on 1st July, 2014 at a cost of ₹ 1,40,000 with CGST and SGST @ 6% each and spent ₹ 10,000 on its installation. The firm writes-off depreciation at 10% of the original cost every year. The books are closed on 31st December every year. Show the Machinery Account and Depreciation Account for three years. [6]

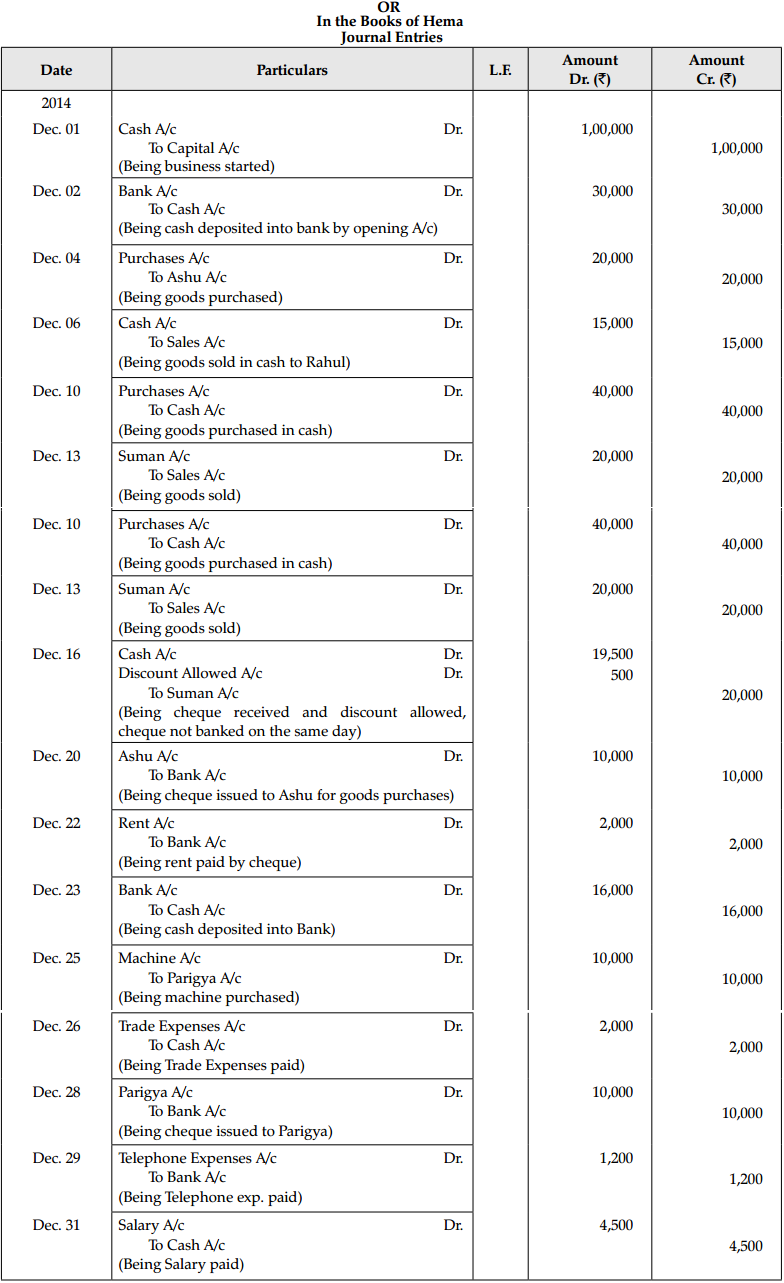

OR

Journalize the following transactions:

| Date | Particulars | ₹ |

| 2014 | 1,00,000 | |

| Dec. 01. | Hema started Business with cash | 30,000 |

| Dec. 02. | Opened a Bank account with SBI | 20,000 |

| Dec. 04. | Purchased goods from Ashu | 15,000 |

| Dec. 06. | Sold goods to Rahul for cash | 40,000 |

| Dec. 10. | Bought goods from Tara for cash | 20,000 |

| Dec. 13. | Sold goods to Suman | 19,500 |

| Dec. 16. | Received cheque from Suman | 500 |

| Discount allowed | 10,000 | |

| Dec. 20. | Cheque given to Ashu on account | 2,000 |

| Dec. 22. | Rent paid by cheque | 16,000 |

| Dec. 23. | Deposited into bank | 10,000 |

| Dec. 25. | Machine purchased from Parigya | 2,000 |

| Dec. 26. | Trade expenses | 10,000 |

| Dec. 28. | Cheque issued to Parigya | 1,200 |

| Dec. 29. | Paid telephone expenses by cheque | 4,500 |

| Dec. 31. | Paid salary | 1,00,000 |

Answer:

Question 22.

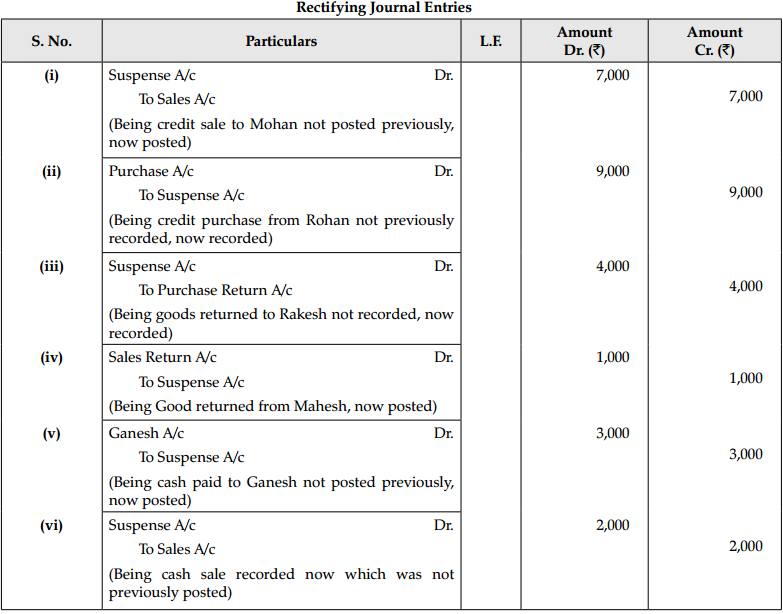

Rectify the following errors and ascertain the amount of difference in trial balance by preparing suspense account:

(i) Credit sales to Mohan ₹ 7,000 were not posted in Sales A/c.

(ii) Credit purchases from Rohan ₹ 9,000 were not posted in Purchase A/c.

(iii) Goods returned to Rakesh ₹ 4,000 were not posted in Purchase Return A/c.

(iv) Goods returned from Mahesh ₹ 1,000 were not posted in Sales Return A/c.

(v) Cash paid to Ganesh ₹ 3,000 was not posted to his account. [6]

(vi) Cash sales ₹ 2000 were not posted.

OR

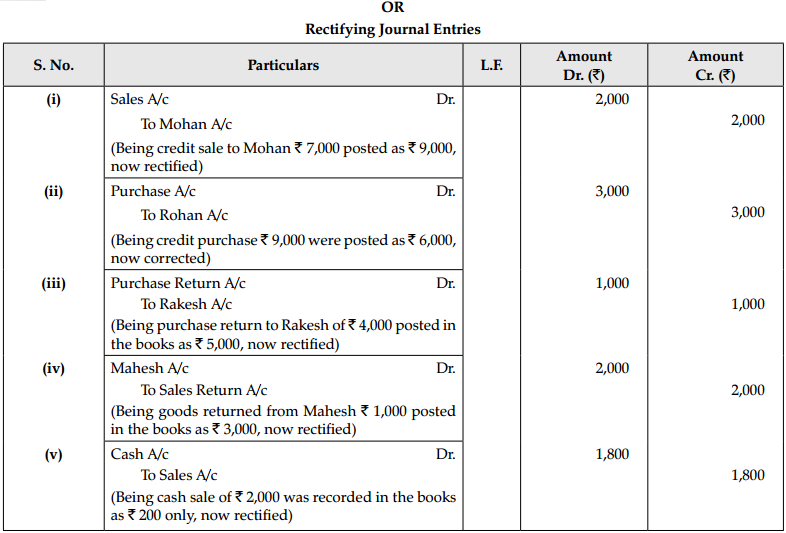

Rectify the following errors:

(i) Credit sales to Mohan ₹ 7,000 were posted as ₹ 9,000.

(ii) Credit purchases from Rohan ₹ 9,000 were posted as ₹ 6,000.

(iii) Goods returned to Rakesh ₹ 4,000 were posted as ₹ 5,000.

(iv) Goods returned from Mahesh ₹ 1,000 were posted as ₹ 3,000.

(v) Cash sales ₹ 2,000 were posted as ₹ 200.

Answer:

Question 23.

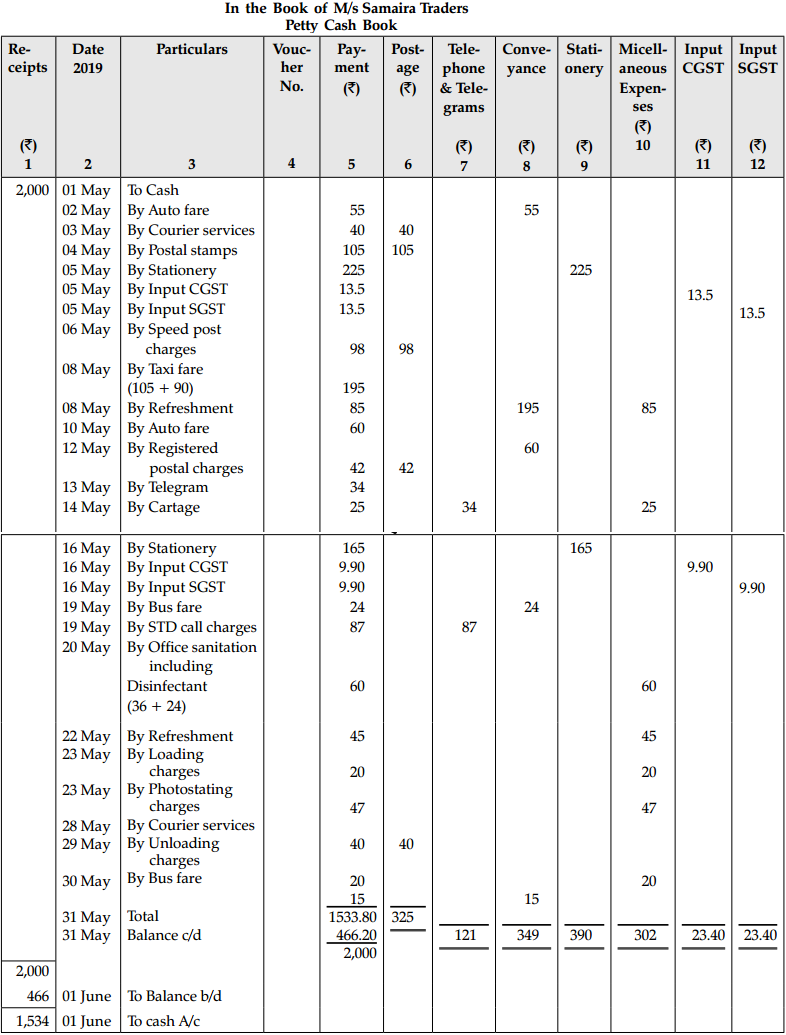

Mr. Mohit, the petty cashier of M/s Samaira Traders received ₹ 2,000 on May 01, 2014 from the Head Cashier. For the month, details of petty expenses are listed here under:

Prepare the Petty Cash Book of M/s Samaira Traders.

| 2019 | Particulars | ₹ |

| May 02 | Auto fare | 55 |

| May 03 | Courier services | 40 |

| May 04 | Postal stamps | 105 |

| May 05 | Stationery ₹ 225 plus CGST and SGST @ 6% each | |

| May 06 | Speed post charges | 98 |

| May 08 | Taxi fare (105 + 90) | 195 |

| May 08 | Refreshments | 85 |

| May 10 | Auto fare | 60 |

| May 12 | Registered postal charges | 42 |

| May 13 | Telegram | 34 |

| May 14 | Cartage | 25 |

| May 16 | Stationery ₹ 165 plus CGST and SGST @ 6% each | |

| May 19 | Bus fare | 24 |

| May 19 | STD call charges | 87 |

| May 20 | Office sanitation including disinfectant (36 + 24) | 60 |

| May 22 | Refreshment | 45 |

| May 23 | Loading charges | 20 |

| May 23 | Photocopying charges | 47 |

| May 28 | Courier services | 40 |

| May 29 | Unloading charges | 20 |

| May 30 | Bus fare | 15 |

Answer:

Question 24.

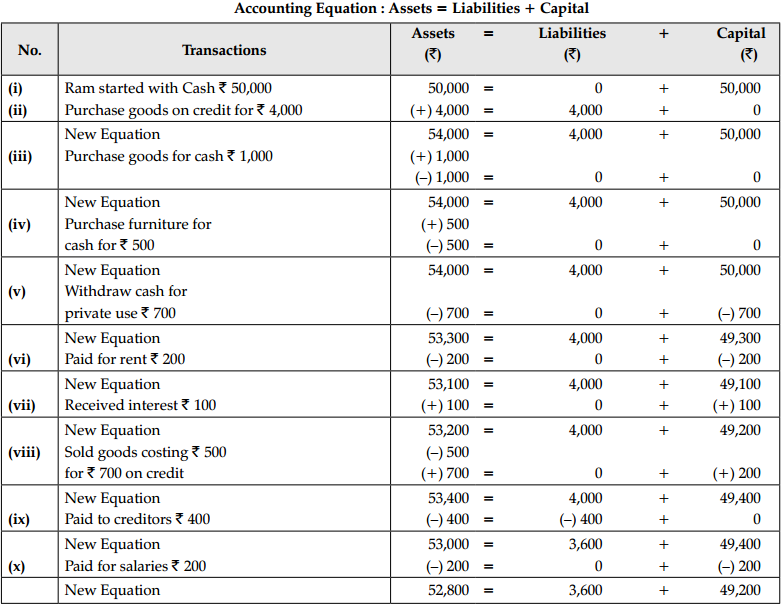

Prepare accounting equation on the basis of the following transactions:

| Particulars | ₹ |

| (i) Ram started business with cash | 50,000 |

| (ii) Purchased goods on credit | 4,000 |

| (iii) Purchased goods for cash | 1,000 |

| (iv) Purchase furniture for cash | 500 |

| (v) Withdrawal for private use | 700 |

| (vi) Paid rent | 200 |

| (vii) Received interest | 100 |

| (viii) Sold goods on credit (cost ₹ 500) | 700 |

| (ix) Paid to creditors | 400 |

| (x) Paid salaries | 200 |

Answer:

Part – B (Financial Accounting – II)

Question 25.

Purpose of Income statement is:

(A) To know the exact financial position of the business on a specified date.

(B) To present a periodical review of financial performance and the financial position of a business enterprise.

(C) To ascertain the profit earned by the business during a specified period.

(D) All the above [1]

OR

Rahul’s trial balance provides you the following information :

Debtors ₹ 80,000 Bad debts ₹ 2,000

Provision for doubtful debts ₹ 4,000

It is desired to maintain a provision for bad debts of ₹ 1,000 State the amount to be debited/credited in Profit and Loss Account:

(A) ₹ 5,000 (Debit)

(B) ₹ 3,000 (Debit)

(C) ₹ 1,000 (Credit)

(D) None of these [1]

Answer:

(C) To ascertain the profit earned by the business during a specified period.

Explanation: Balance Sheet reflects the financial position whereas Income Statement/ Profit and Loss Account tells about the financial performance.

OR

(A) ₹ 5,000 (Debit)

Question 26.

All types of accounts are not shown in Balance Sheet. Which type of the accounts are shown in it ?

(A) Real Account

(B) Personal Account

(C) Both (A) and (B)

(D) Neither (A) nor (B) [1]

Answer:

(C) Both (A) and (B)

Explanation: All Real and Personal Accounts are shown in the Balance Sheet but all the nominal accounts are shown in the Trading and Profit and Loss Account.

Question 27.

Statement I: Interest on drawings to be deducted from capital in the liabilities side in the balance sheet. Statement II: The income which has become due but not yet received in cash is called accrued income.

(A) Both Statements are correct.

(B) Both Statements are incorrect.

(C) Statement I is correct and Statement II is incorrect.

(D) Statement I is incorrect and Statement II is correct. mm

OR

……………… is a statement to know the exact financial position of the business on a specified date.

(A) Position Statement

(B) Income Statement

(C) Profit and Loss Appropriation Account

(D) None of the above [1]

Answer:

(A) Both Statements are correct.

OR

(B) Income Statement

Question 28.

Which of the following is correct?

(A) Operating profit = Operating profit – Non-operating expenses – Non-operating incomes

(B) Operating profit = Net profit + Non-operating expenses + Non – operating incomes

(C) Operating profit = Net profit + Non-operating expenses – Non – operating incomes

(D) Operating profit = Net profit – Non-operating expenses + Non-operating incomes [1]

Answer:

(C) Operating profit = Net profit + Non-operating expenses – Non – operating incomes

Question 29.

Identify the adjustment for prepaid expenses:

(A) Added to expenses in Trading and Profit & Loss Account and shown in liabilities side of Balance Sheet.

(B) Deducted from expenses in Trading and Profit & Loss Account and shown in assets side of Balance Sheet.

(C) Added to expenses in Trading and Profit & Loss Account and shown in assets side of Balance Sheet.

(D) Deducted from expenses in Trading and Profit & Loss Account and shown in liabilities side of Balance sheet. [1]

Answer:

(B) Deducted from expenses in Trading and Profit & Loss Account and shown in assets side of Balance Sheet.

Question 30.

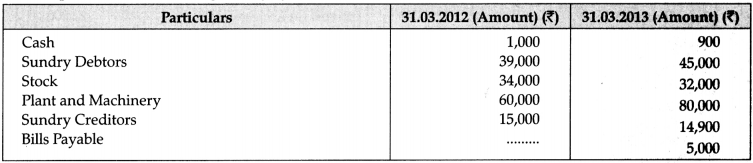

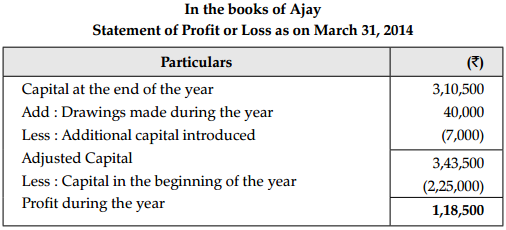

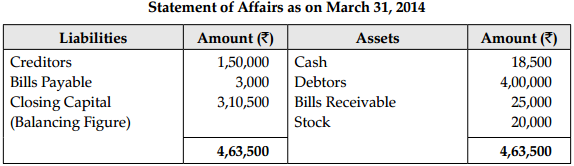

Ajay started business with a capital of ₹ 2,25,000 on 1st April, 2013. During the year he withdrew ₹ 40,000 for his personal use and introduced ₹ 7,000 as fresh capital. On 31st March, 2014, his position of assets and liabilities stood as follows:

| Particulars | ₹ |

| Cash-in-hand | 18,500 |

| Stock | 20,000 |

| Bills Receivable | 25,000 |

| Debtors | 4,00,000 |

| Creditors | 1,50,000 |

| Bills Payable | 3,000 |

You are required to prepare statement of profit or loss for the year ended 31 March, 2014. [3]

OR

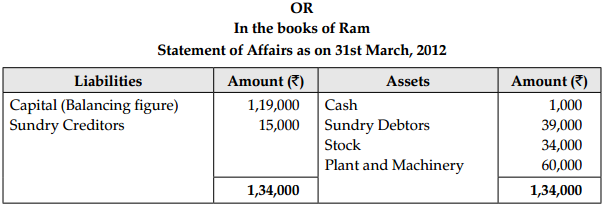

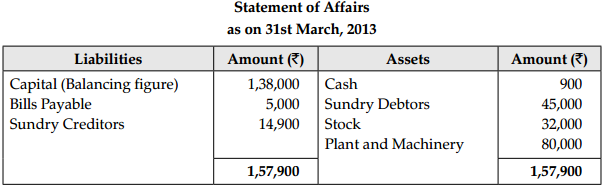

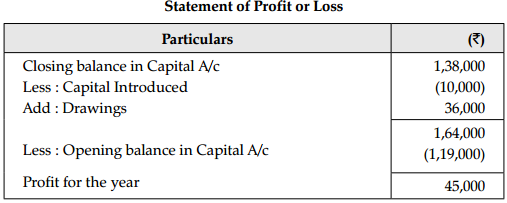

Ram keeps his books under Single Entry System. His Assets and Liabilities were as under:

During 2012-13, he introduced ? 10,000 as new Capital. He withdrew ? 3,000 every month for his household expenses. Ascertain his profit for the year ended 31st March, 2013.

Answer:

Question 31.

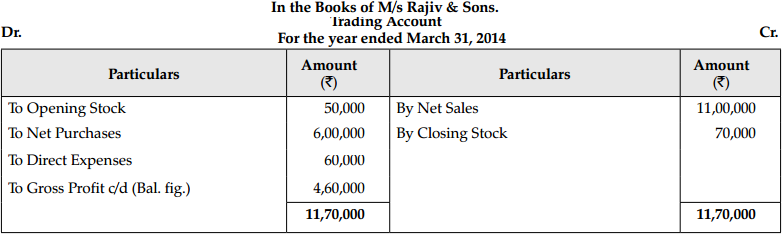

Calculate the amount of Gross Profit and Operating Profit on the basis of the following balances extracted from the books of M/s Rajiv and Sons for the year ended March 31,2014:

| Particulars | ₹ |

| Opening stock | 50,000 |

| Net sales | 11,00,000 |

| Net purchases | 6,00,000 |

| Direct expenses | 60,000 |

| Administration expenses | 45,000 |

| Selling and distribution expenses | 65,000 |

| Loss due to fire | 20,000 |

| Closing stock | 70,000 |

Answer:

Operating Profit = Sales – (Opening Stock + Net Purchases + Direct Expenses + Administration Expenses + Selling and Distribution Expenses) + Closing Stock

= ₹ 11,00,000 – ₹ (50,000 + ₹ 6,00,000 + ₹ 60,000 + ₹ 45,000 + ₹ 65,000) + ₹ 70,000 = ₹ 3,50,000

OR

Operating Profit = Gross Profit – Operating Expenses + Operating Income = 4,60,000 – 45,000 – 65,000 = 3,50,000

Question 32.

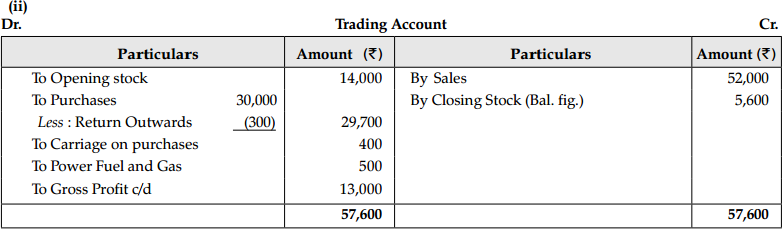

From the following particulars, you are required to find:

(i) Cost of Goods Sold

(ii) Closing Stock

| Particulars | ₹ |

| Purchases | 30,000 |

| Sales | 52,000 |

| Opening Stock | 14,000 |

| Salaries and Wages | 3,000 |

| Carriage Inwards | 400 |

| Returns Outward | 300 |

| Power, fuel and gas | 500 |

| Rate of Gross Profit is 25% of Sales |

Answer:

(i) Sales = ₹ 52,000

Gross Profit = 25% of ₹ 52,000 = ₹ 13,000

Cost of Goods Sold = Sales – Gross Profit

= ₹52,000 – ₹ 13,000 = ₹ 39,000

Question 33.

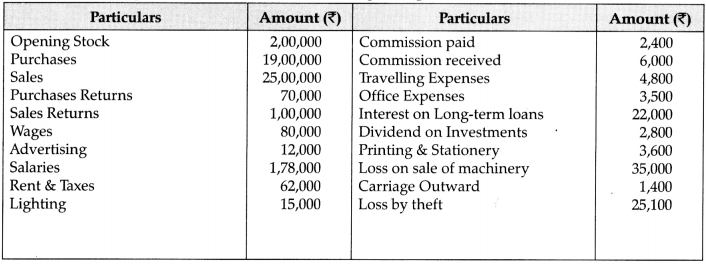

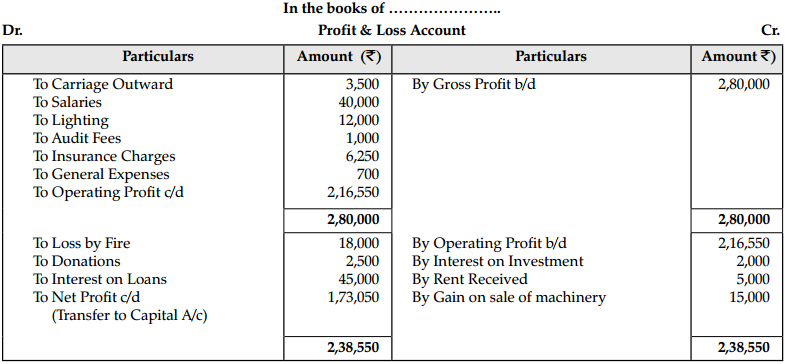

Find out the Operating Profit and Net Profit from the following information:

| Gross Profit | ₹ |

| Carriage Outward | 2,80,000 |

| Salaries | 3,500 |

| Lighting | 40,000 |

| Audit Fees | 12,000 |

| Interest on Investments | 1,000 |

| Rent Received | 2,000 |

| Loss by fire | 5,000 |

| Donation | 18,000 |

| Insurance Charges | 2,500 |

| General Expenses | 6,250 |

| Gain on sale of machinery | 700 |

| Interest on loans | 15,000 |

OR

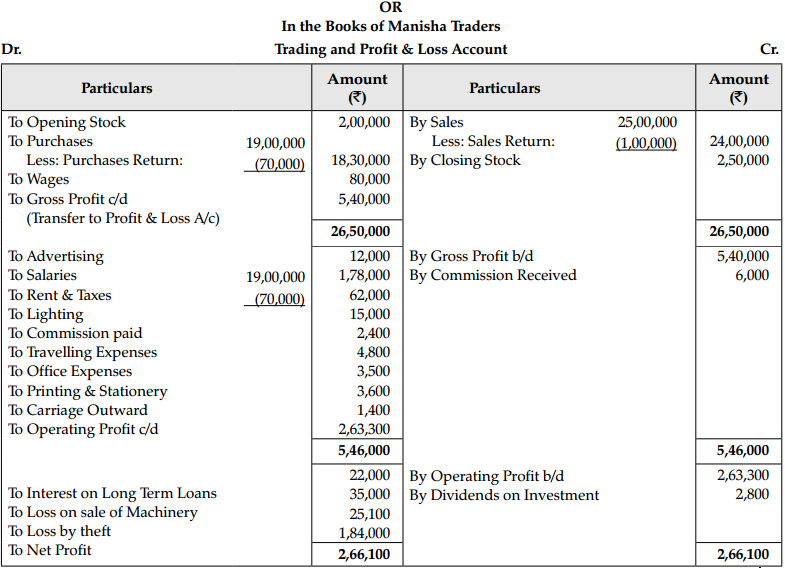

From the following particulars calculate Gross Profit, Operating Profit and Net Profit of Manisha Traders:

Closing stock was valued at ₹ 2,50,000.

Answer:

Question 34.

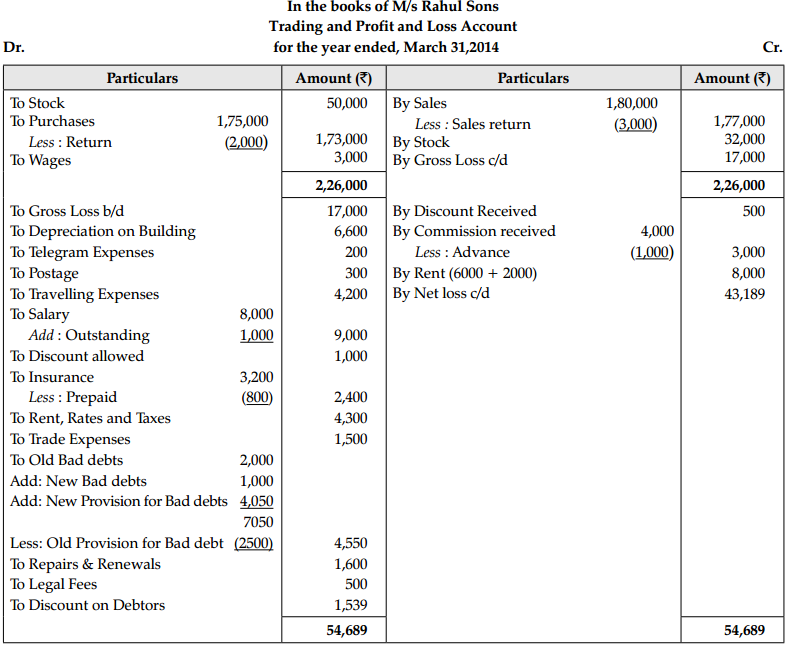

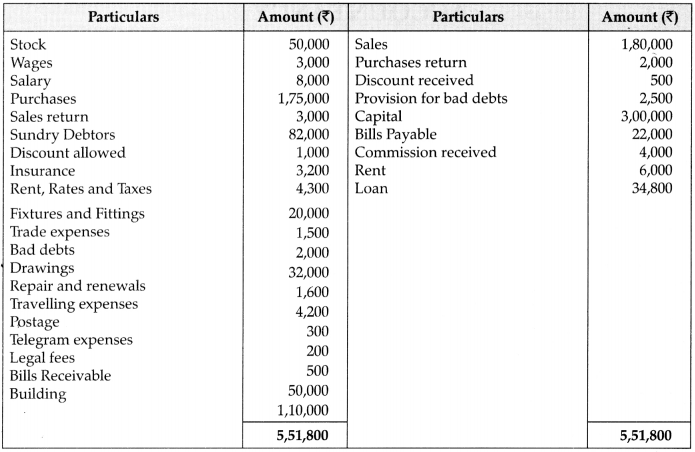

Prepare a Trading and Profit and Loss Account for the year ending March 31, 2014, from the balances extracted of M/s Rahul Sons. Also, prepare a balance sheet at the end of the year.

Adjustments:

(i) Commission received in advance 1,000.

(ii) Rent receivable 2,000.

(iii) Salary outstanding 1,000 and insurance prepaid 800.

(iv) Further bad debts 1,000 and provision for bad debts @ 5% on debtors and discount on debtors @ 2%.

(v) Closing stock 32,000.

(vi) Depreciation on building @ 6% p.a.

Answer: