Students can access the CBSE Sample Papers for Class 11 Accountancy with Solutions and marking scheme Set 2 will help students in understanding the difficulty level of the exam.

CBSE Sample Papers for Class 11 Accountancy Set 2 with Solutions

Time Allowed : 3 hours

Maximum Marks: 70

General Instructions:

- This question paper contains 34 questions. All questions are compulsory.

- This question paper is divided into two parts, Part A and B.

- Question Nos. 1 to 15 and 25 to 29 carries 1 mark each.

- Questions Nos. 16 to 18,30 to 32 carries 3 marks each.

- Questions Nos. 19,20 and 33 carries 4 marks each

- Questions Nos. from 21 to 24 and 34 carries 6 marks each

- There is no overall choice. However, an internal choice has been provided in 7 questions of one mark, 2 questions of three marks, 1 question of four marks and 2 questions of six marks

Part – A ((Financial Accounting – I)

Question 1.

Which is the first step of accounting process?

(A) Identification of business transaction

(B) Posting to ledger

(C) Analysis and Interpretation

(D) Communicating the results

Answer:

(A) Identification of business transaction

Question 2.

Assertion: Under cash basis of accounting, transactions are entered when actual cash is received or paid out. [1]

Reason: This system of recording does not take into account outstanding expenses or accrued income for a current year.

(A) Both A and R are correct, and R is the correct explanation of A.

(B) Both A and R are correct, but R is not the correct explanation of A.

(C) A is correct, but R is incorrect.

(D) A is incorrect, but R is correct. [1]

Answer:

(B) Both A and R are correct, but R is not the correct explanation of A.

Question 3.

Consider the following statements with regard to the advantages of Cash basis of Accounting:

(i) Accounting under this method is simple as adjustments for outstanding expenses, prepaid expenses are not required.

(ii) Recognized under the Companies Act and used more widely by business enterprises.

(iii) It is more objective as use of personal judgments and estimates are minimized.

Identify the correct statement/statements:

(A) (i) and (iii)

(B) (ii) only

(C) (i),and(ii)

(D) (i), (ii) and (iii) [1]

OR

The accounting concept that refers to the tendency of accountants to resolve uncertainty and doubt in favour of

understating assets and revenues and overstating liabilities and expenses is known as .

(A) Matching

(B) Conservatism

(C) Revenue Realisation

(D) Consistency [1]

Answer:

(A) (i) and (iii)

Explanation: Accrual basis of accounting is the one accepted by the statute of the country.

OR

(B) Conservatism

Explanation: The principle of conservatism requires a business to be extremely cautious about possible losses. It should guard against any possible losses. If there is an anticipated loss, there should be adequate provision in the account. There need not to be any provision for anticipated revenue or gain.

Question 4.

It may be referred to as the amount (in terms of money or assets having money value) which is invested by the owner(s) in the business. A proprietor or partner can claim his share from the firm if the business is closed or a partner retires. What are we talking about?

(A) Loan

(B) Capital

(C) Bills Receivable

(D) Cash in Hand [1]

OR

A bill of exchange, when accepted by a debtor is called a .

(A) Bills Receivable

(B) Bills Payable

(C) Both (A) and (B)

(D) Neither,(A) nor (B) [1]

Answer:

(B) Capital

OR

(A) Bills Receivable

Question 5.

Pick the odd one out:

(A) Bank Loan

(B) Cash at Bank

(C) Creditors

(D) Bills Payable [1]

Answer:

(B) Cash at Bank

Explanation: Cash at bank is an asset whereas rest are liabilities of the business.

Question 6.

A concept that a business enterprise will not be sold or liquidated in the near future is known as:

(A) Going concern

(B) Economic entity

(C) Monetary unit

(D) None of the these [1]

OR

Consider the following statements:

(i) Accounting standards provide the norms on the basis of which financial statements should be prepared.

(ii) Accounting standards ensure uniformity in the preparation and presentation of financial statements by removing the effect of diverse accounting practices.

(iii) Accounting standards provide a useful system to resolve potential financial conflicts of interest between various groups.

(iv) Accounting standards help auditors in the audit of accounts. Accounting standards raise standard of audit of accounts.

Identify the correct statement/s which state the purpose of accounting standards.

(A) (i), (iii) and (iv)

(B) (ii), (iii) and (iv)

(C) (i), (ii), (iii) and (iv)

(D) (i), (ii) and (iii) [1]

Answer:

(A) Going concern

Explanation: The concept of going concern assumes that a business firm would continue to carry out its operations indefinitely, i.e. for a fairly long period of time and would not be liquidated in the foreseeable future. This is an important assumption of accounting as it provides the very basis for showing the value of assets at their original cost and they are depreciated in a systematic manner over their expected useful life in the balance sheet.

OR

(C) (i), (ii), (iii) and (iv)

Question 7.

Assertion: Accounting standards are needed to ensure uniformity in the preparation and presentation of financial statements.

Reason: Accounting standards make accounting procedures universally acceptable by removing the diverse accounting practices and policies.

(A) Both A and R are correct, and R is the correct explanation of A.

(B) Both A and R are correct, but R is not the correct explanation of A.

(C) A is correct, but R is incorrect.

(D) A is incorrect, but R is correct.

Answer:

(B) Both A and R are correct, but R is not the correct explanation of A.

Question 8.

What are the documents called which provide evidence of the transactions?

(A) Source documents

(B) Voucher

(C) Both (A) and (B)

(D) None of the these

OR

Outstanding rent is a ………………. account.

(A) Real

(B) Nominal

(C) Personal

(D) Expense

Read the following hypothetical situation, answer question nos. 9 and 10.

The cash book of Ramesh showed the cash balance of ₹15,000 and a bank balance of ₹ 25,000 as on 30th April, 2019. On the 1st of May, he purchased goods worth ₹ 12,000 and paid it by cheque. He sold goods on 3rd of May for cash and deposited the proceeds into bank worth ₹10,000. On the 14th of May, he paid the electricity bill by cheque worth ₹ 9,000. On the 15th of May from Rashi, he purchased goods worth ₹ 10,000 at a discount of 20% and sold it to Juhi at a profit of 25%. Both the transactions were on credit. On the 26th of May, he withdrew ₹ 5,000 for office use. On 29th May, he received 70%of the cash from Juhi and paid 50% of it to Rashi and deposited the remaining in the bank. He also paid ₹ 1,500 as salaries to his employee on 31st of May. He also had the following transactions:

He received a telephone bill worth ₹ 500.

He withdrew ₹ 2,500 for his personal use.

He gave ₹ 500 from for the cash register to his nephew as a gift.

Goods worth ₹ 2,000 were lost due to damages.

Answer:

(C) Both (A) and (B)

Explanation: Business transactions are usually evidenced by an appropriate document such as Cash memo, Invoice, Sales bill, Pay-in-slip, Cheque, Salary slip, etc. A document which provides evidence of the transactions on the basis of which entries are made in subsidiary books is termed as Source Document or a Voucher.

OR

(C) Personal

Question 9.

Where will the transaction of 1st of May recorded?

(A) Cash Column

(B) Bank Column

(C) Discount Column

(D) petty Cash Book

Answer:

(B) Bank Column

Question 10.

There will be a contra entry for the transaction on which date?

(A) 3rd of May

(B) 15th of May

(C) 26th of May

(D) Capital

Answer:

(D) Capital

Question 11.

………………. are probable liabilities which are dependent on happening of a certain event.

(A) Contingent Liability

(B) Current Liability

(C) Non-current Liability

(D) Capital [1]

Answer:

(A) Contingent Liability

Explanation: Contingent liabilities are not actual liabilities. They are probable liabilities which are dependent on the happening of a certain contingency. For example, a claim against the business in court is a contingent liability. If the court decides against the business, the claim becomes a real liability to pay. Other examples of contingent liabilities are loan guaranteed by the business, bills receivable discounted with the bank, etc.

Question 12.

Consider the following statements with regard to the imprest system of maintaining petty cash book:

(i) A fixed amount is advanced to the petty cashier to make the payments.

(ii) The amount given to the petty cashier is known as’imprest amount’.

(iii) The amount is determined on the basis of past experience in such a way that it will be sufficient to meet the requirements for a given period.

(iv) The period is a month only.

Identify the correct statement/statements:

(A) (i) and (iii)

(B) (i), (ii) and (iii)

(C) (i) and (iv)

(D) (i), (ii) and (iv)

Answer:

(B) (i), (ii) and (iii)

Question 13.

Accrual concept applies equally to ………….. and …………..

(A) Revenue, Expenses

(B) Income, Payments

(C) Receipts, Payments

(D) All of the these

Answer:

(D) All of the these

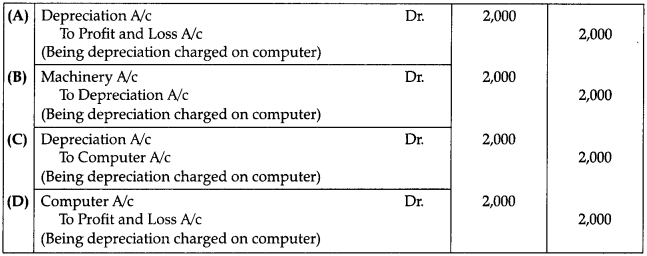

Question 14.

Anu charges 10% depreciation on the computers, book value being ₹ 20,000. Pass the journal entry?

Answer:

Option (C) is correct.

Question 15.

What does the right side of the Cash Book show?

(A) Payments in cash

(B) Expenses and losses

(C) Both (A) and (B)

(D) None of the these [1]

OR

Consider the following statements with respect to the functions of Journal: ,

(i) Transactions are analysed according to the debit and credit aspect, thereby finding out how each transaction will financially affect the business.

(ii) Transactions are recorded with a brief narration that explains the transaction in simple language.

(iii) It contains a chronological record of transactions on the basis of assumptions

Identify the correct statement/statements:

(A) (i) and (ii)

(B) (ii) and (iii)

(C) (i) and (iii)

(D) (i), (ii) and (iii) [1]

Answer:

(A) Payments in cash

Explanation: Expenses and losses can be of credit nature so not necessarily be recorded in the cash book as cash book will record only cash transactions.

OR

(A) (i) and (ii)

Question 16.

Discuss the advantages or benefits of accounting standards. [3]

OR

Explain the following:

(i) Accounting Standards

(ii) Matching Concept

(iii) Going Concern Assumption.

Answer:

Following are the benefits of accounting standards :

(i) Creditability and Reliability of Financial Statement: Accounting standards provide a structured framework within which credible financial statements can be produced. Accounting standards standardize diverse accounting policies and practices and eliminate the non-comparability of financial statements.

(ii) Beneficial to Accountants and Auditors: Accounting standards provide the norms on the basis of which business transactions are recorded and financial statements are prepared. Accountants are not required to use personal judgement and discretion while recording business transactions. Accounting standards helps the auditors in the audit of accounts.

(iii) Managerial Accountability: Accounting standards help in assessing managerial skills in ensuring profitability of the enterprise and in measuring the effectiveness of management s stewardship. It will be difficult for the management to manipulate financial data.

(iv) Development of Accounting Theory: Accounting standards provide a coherent, logical, conceptual framework and structure for accounting measurements, financial reporting and usefulness of accounting data. This has facilitated the making of accounting theory which commands universal acceptance

OR

(i) Accounting Standards: Accounting Standards are the guidelines for financial accounting, such as, how a firm prepares and presents its business income, expenses, assets and liabilities. The main purpose of accounting standards is to promote a better understanding of financial statements.

(ii) Matching Concept: The matching principle is one of the basic underlying guidelines in accounting. The main purpose of the principle is to direct a company to report an expense on its income statement in the same period as the related revenues. Matching concept also requires the application

of personal judgment in making the estimated for doubtful debts, discount, etc.

(iii) Going Concern Assumption: This concept assumes that every business has a long and indefinite life. Since

financial statements are prepared on the basis of this concept, all fixed assets are shown in the books at their cost ignoring their market value.

Question 17.

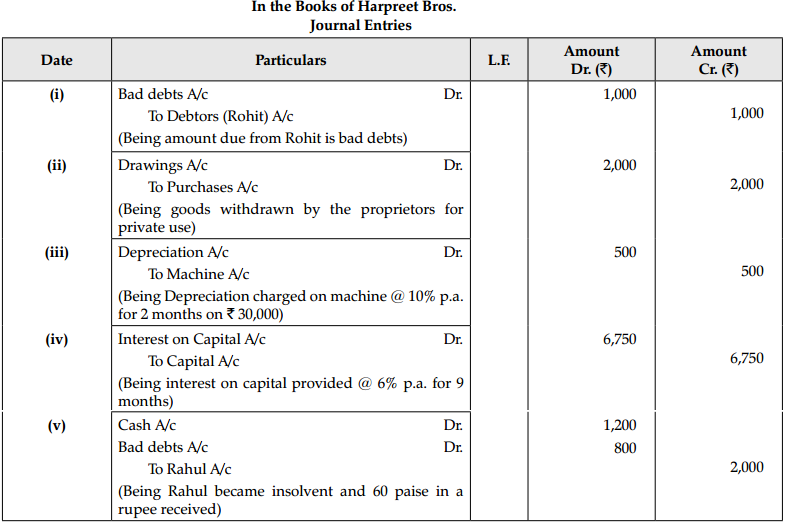

Journalise the following transactions in the books of Harpreet Bros:

(i) ₹ 1,000 due from Rohit are now a bad debts

(ii) Goods worth ₹ 2,000 were used by the proprietor.

(iii) Charge depreciation @ 10% p.a. for two month on machine costing ₹ 30,000.

(iv) Provide interest on Capital of ₹ 1,50,000 at 6% p.a. for 9 months.

(v) Rahul became insolvent, who owed ₹ 2,000. A final dividend of 60 paise in a rupee is received from his estate. [3]

Answer:

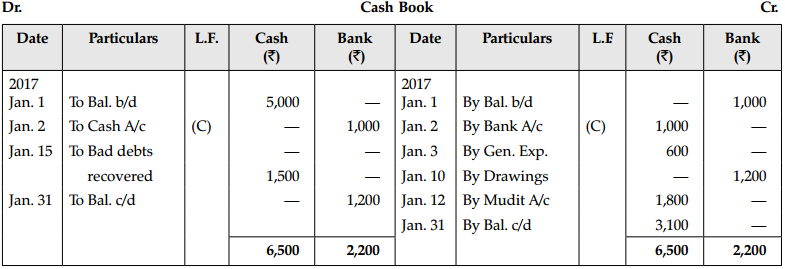

Question 18.

Prepare a Cash Book with Cash and Bank Columns from the following transactions:

| 2017 | Particulars | ₹ |

| Jan. 1 | Cash in hand ₹ 5,000, Bank overdraft ₹ 1,000 | |

| Jan. 2 | Deposited into bank | 1,000 |

| Jan. 3 | General Expenses paid | 600 |

| Jan. 7 | Purchased goods from Mudit on credit | 2,000 |

| Jan.10 | Drew from bank for personal use | 1200 |

| Jan. 12 | Paid to Mudit in full settlement | 1,800 |

| Jan. 15 | Recovered from Sunny, who owes ₹ 3,000 and money had been recorded as bad debts | 1,500 |

Answer:

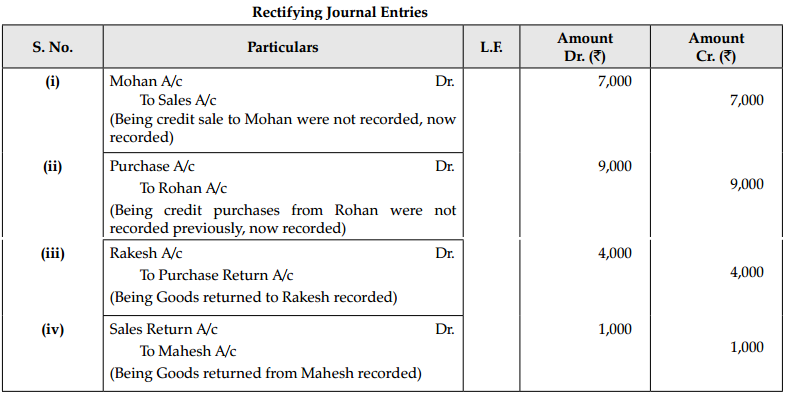

Question 19.

Rectify the following errors:

(i) Credit sales to Mohan ₹ 7,000 were not recorded.

(ii) Credit purchases from Rohan ₹ 9,000 were not recorded.

(iii) Goods returned to Rakesh ₹ 4,000 were not recorded.

(iv) Goods returned from Mahesh ₹ 1,000 were not recorded. [4]

Answer:

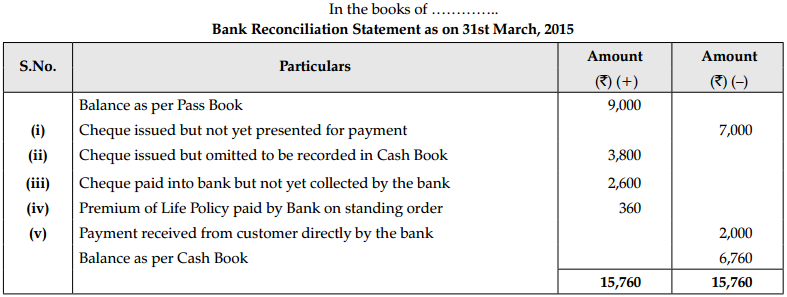

Question 20.

On 31st March, 2015 the pass book showed a credit balance of ₹ 9,000. Prepare a Bank Reconciliation Statement from the following particulars :

(i) Cheque issued but not yet presented for payment ₹ 7,000.

(ii) Cheque issued but omitted to be recorded in cash book ₹ 3,800.

(iii) Cheque paid into bank but not yet collected by the bank ₹ 2,600.

(iv) Premium of life policy paid by bank on standing order ₹ 360

(v) Payment received from customers directly by the bank ₹ 2,000.

Answer:

Question 21.

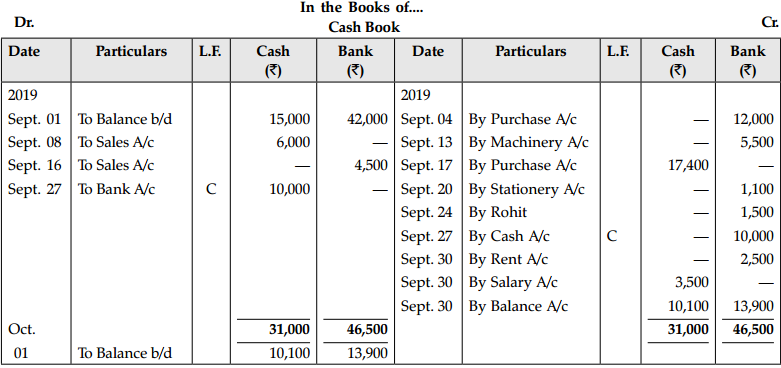

Enter the following transactions in Cash Book with bank column:.

| 2019 | Particulars | ₹ |

| Sept. 01 | Bank balance | 42,000 |

| Sept. 01 | Cash balance | 15,000 |

| Sept. 04 | Purchased goods by cheque | 12,000 |

| Sept. 08 | Sale of goods for cash | 6,000 |

| Sept. 13 | Purchased machinery by cheque | 5,500 |

| Sept. 16 | Sold goods and received cheque (deposited on same day) | 4,500 |

| Sept. 17 | Purchased goods from Mridula in cash | 17,400 |

| Sept. 20 | Purchased stationery by cheque | 1,100 |

| Sept. 24 | Cheque given to Rohit | 1,500 |

| Sept. 27 | Cash withdrawn from bank | 10,000 |

| Sept. 30 | Rent paid by cheque | 2,500 |

| Sept. 30 | Paid salary | 3,500 |

OR

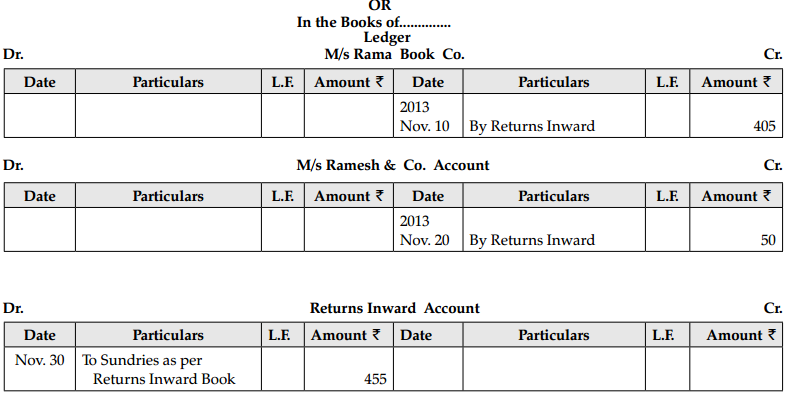

Post the following into the Ledger:

Answer:

Question 22.

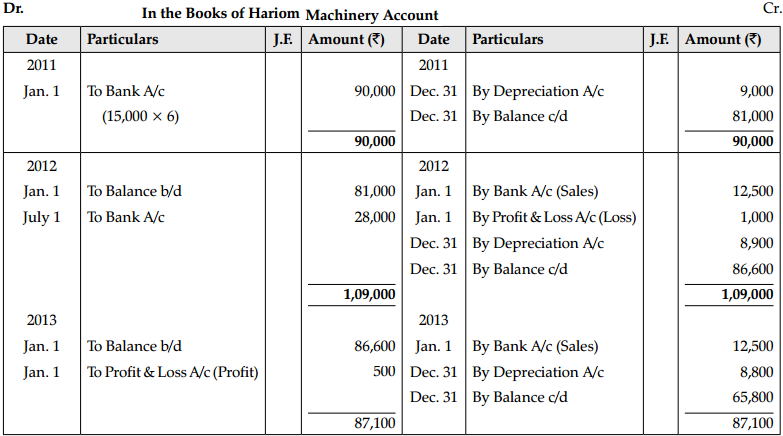

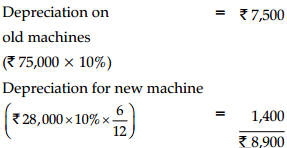

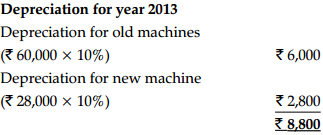

On 1st January, 2011 Hari Om purchased 6 machines @ ₹ 15,000 each. His accounting year ends on 31st December. Depreciation at the rate of 10% p.a. on original cost was to be charged. On 1st January, 2012 one machine was sold for ₹ 12,500 and on 1st January, 2013 a second machine was sold for ₹ 12,500. An improved model which cost ₹ 28,000 was purchased on 1st July, 2012. Show Machine Account till 2013. [6]

OR

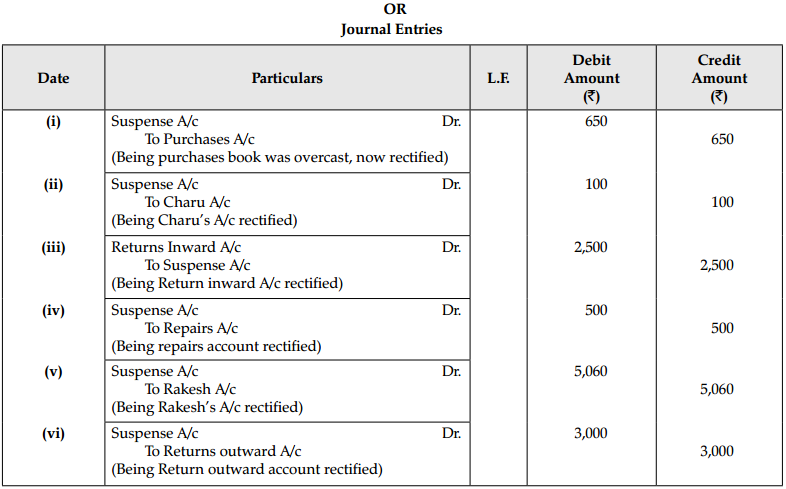

Rectify the following errors which were detected before making the Trial Balance:

(i) Purchases Book has been overcast by ₹ 650.

(ii) A discount of ₹ 100 allowed to Charu has not been posted to her account.

(iii) Returns Inward of ₹ 2,500 has not been posted to Returns Inward A/c.

(iv) A payment of ₹ 500 as repairs has been debited to Repairs A/c twice.

(v) Goods purchased from Rakesh for ₹ 4,600 on credit has been correctly entered in the Purchases Book but it has been debited to his account as ₹ 460.

(vi) Returns Outward of ₹ 3,560 has been posted to Returns Outward Account as ₹ 560. [6]

Answer:

Working Notes :

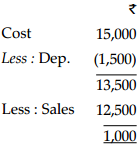

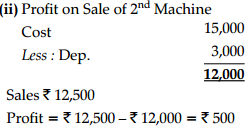

(i) Loss On sale of 1 st Machine

(iii) Depreciation for the year 2012

(iv)

Question 23.

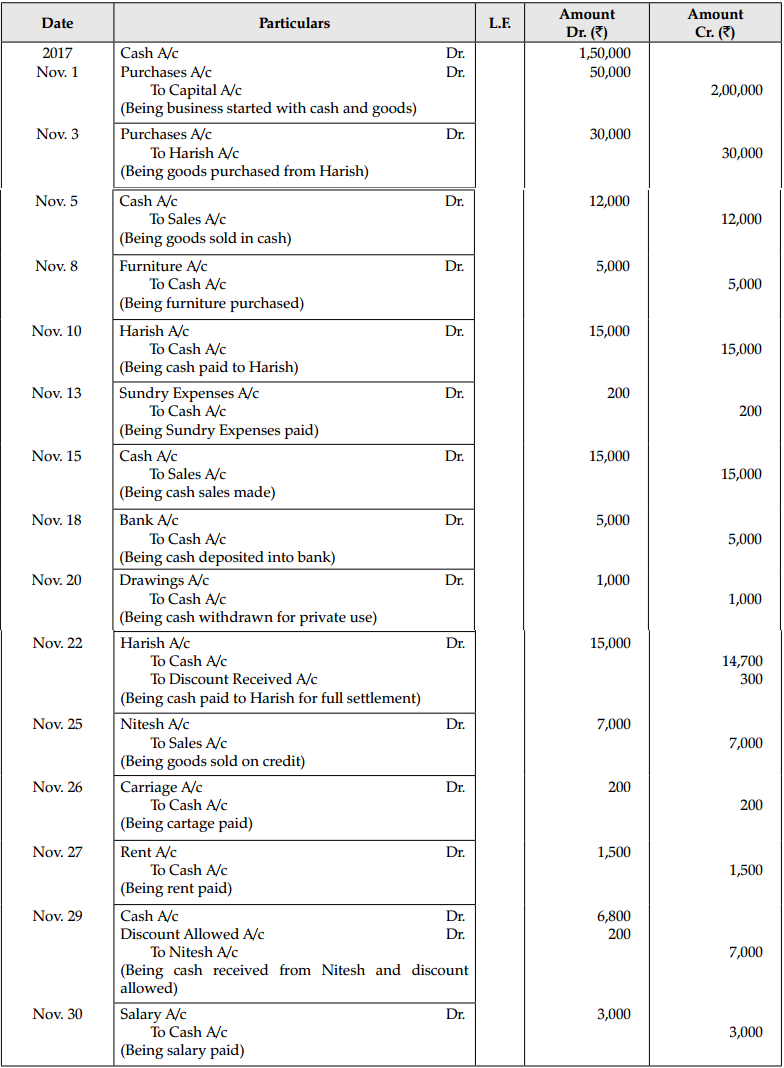

Journalise the following transactions:

| Date | Particulars | ₹ |

| 2017 | – | |

| Nov. 1 | Business started with Cash | 1,50,000 |

| Goods | 50,000 | |

| Nov. 3 | Purchased goods from Harish | 30,000 |

| Nov. 5 | Sold goods for cash | 12,000 |

| Nov. 8 | Purchase furniture for cash | 5,000 |

| Nov. 10 | Cash paid to Harish on account | 15,000 |

| Nov. 13 | Paid sundry expenses | 200 |

| Nov. 15 | Cash sales | 15,000 |

| Nov. 18 | Deposited into Bank | 5,000 |

| NOv. 20 | Drew cash for personal use | 1,000 |

| Nov. 22 | Cash paid to Harish in full settlement of account | 14,700 |

| Nov. 25 | Goods sold to Nitesh | 7,000 |

| Nov. 26 | Carriage paid | 200 |

| Nov. 27 | Rent Paid | 1,500 |

| Nov. 29 | Received cash from Nitesh | 6,800 |

| Nov. 30 | Discount given | 200 |

| Nov. 30 | Salary paid | 3,000 |

Answer:

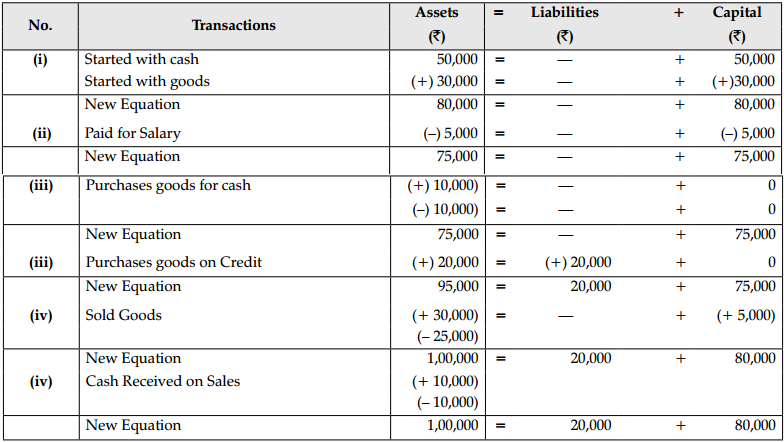

Question 24.

Prepare the accounting equation on the basis of the following transactions:

(i) Commenced business with cash ₹ 50,000 and goods ₹ 130,000

(ii) Paid Salary ₹ 5,000

(iii) Purchased goods for cash ₹ 10,000 and on credit ₹ 20,000

(iv) Goods costing ₹ 25,000 sold at profit of 20% on cost out of which ₹ 10,000 received in cash.

Answer:

Part – B (Financial Accounting – II)

Question 25.

If the rent received in advance is ₹ 2,000, the adjustment entry will be:

(A) Debit Profit and Loss Account and Credit Rent Account

(B) Debit Rent Account Credit rent received in advance account

(C) Debit rent received in advance account and Credit rent account

(D) None of these. [1]

OR

If the insurance premium paid ₹ 1,000, prepaid insurance ₹ 300, the amount of insurance premium shown in Profit and Loss Account will be:

(A) ₹ 1,300

(B) ₹ 1,000

(C) ₹ 300

(D) ₹ 700 [1]

Answer:

(B) Debit Rent Account Credit rent received in advance account

Explanation: We need to debit the rent account as it is a nominal account, and as per the golden rule, in nominal account expenses are debited. We credit the rent in advance account with that amount.

OR

(D) ₹ 700

Explanation: In Profit and Loss Account only that amount is shown that is pertaining to the current year for ascertaining profit or loss of the firm. In such a case prepaid or advance are subtracted and outstanding or arrears are added.

Question 26.

Which of the following expenses means the expenses which have become due during the accounting year but have not been paid:

(A) Capital Expenditure

(B) Revenue Expenditure

(C) Outstanding expenses

(D) Deferred Revenue expenses [1]

Answer:

Option (C) is correct.

Explanation: The expenses pertaining to the current year but not paid are called outstanding. Capital Expenditures are those that are incurred for either creating an asset or reducing a liability. Revenue Expenditures incurred for the day to day functioning of the business.

Question 27.

Statement I: For the preparation of financial statements, it is necessary that all the adjustments arising on accrual basis of accounting are made at the end of the accounting period.

Statement II: Depreciation is the decline in the value of an asset, on account of wear and tear or passage of time.

(A) Both Statements are correct.

(B) Both Statements are incorrect.

(C) Statement I is correct and Statement II is incorrect.

(D) Statement I is incorrect and Statement II is correct.

OR

Which of the following entries are passed to correct the values of accounts shown in the Trial Balance:

(A) Rectification Entries

(B) Adjusting Entries

(C) Both (A) and (B)

(D) None of the above [1]

Answer:

(A) Both Statements are correct.

OR

(B) Adjusting Entries

Question 28.

How will the commission given to the General Manager be adjusted in the Final Accounts?

(A) Debit side of the Trading Account and In the Liability side of the Balance Sheet.

(B) Credit side of the Profit and Loss Account and in the Asset side of the Balance Sheet.

(C) Credit side of the Trading Account and in the Asset side of the Balance Sheet

(D) Debit side of the Profit and Loss Account and in the Liability side of the Balance Sheet. [1]

Answer:

(D) Debit side of the Profit and Loss Account and in the Liability side of the Balance Sheet.

Question 29.

Credit sales can be ascertained as the balancing figure in the account.

(A) Creditors

(B) Debtors

(C) Capital

(D) Statement of Affairs [1]

Answer:

(B) Debtors

Question 30.

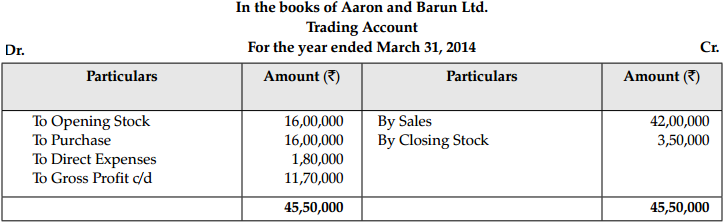

From the following balances taken from the books of Aaron and Barun Ltd. for the year ending March 31,2014, calculate the gross profit.

| ₹ | |

| Closing stock | 3,50,000 |

| Net sales during the year | 42,00,000 |

| Net purchases during the year | 16,00,000 |

| Opening stock | 16,00,000 |

| Direct expenses | 1,80,000 |

OR

Operating profit earned by M/s Ashish and Diksha in 2013-14 was ₹ 27,00,000. Its non-operating incomes were ₹ 1 1,50,000 and non-operating expenses were ₹ 13,75,000. Calculate the amount of net profit earned by the firm. [3]

Answer:

OR

Net Profit = Operating Profit + Non- operating Income – Non-operating Expenses

= 27,00,000 + 11,50,000 – 13,75,000 = ‘ 24,75,000

Net profit earned by M/S Ashish and Diksha in 2013-14 was ‘ 24,75,000

Question 31.

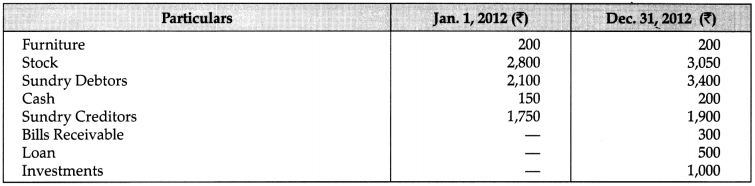

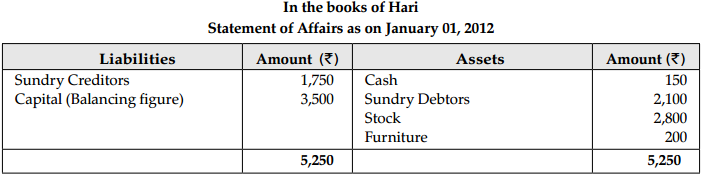

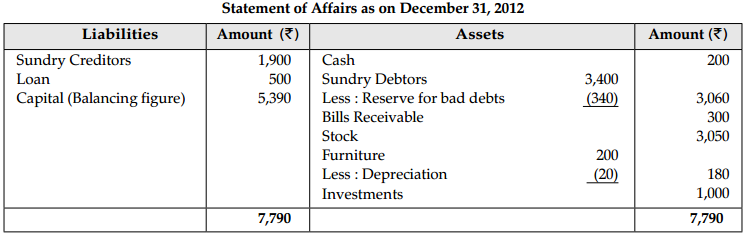

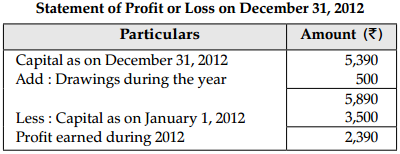

Hari maintains his books of account on single entry system. His books provide the following information:

His drawings during the year was ₹ 500. Depreciate furniture by 10% and provide a reserve for bad debts at 10% on sundry debtors. Calculate profit. [3]

Answer:

Question 32.

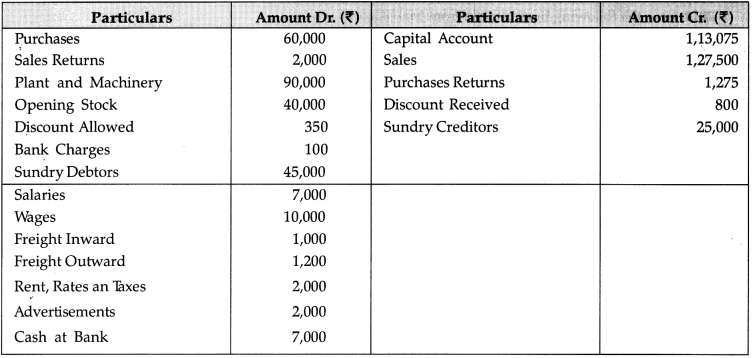

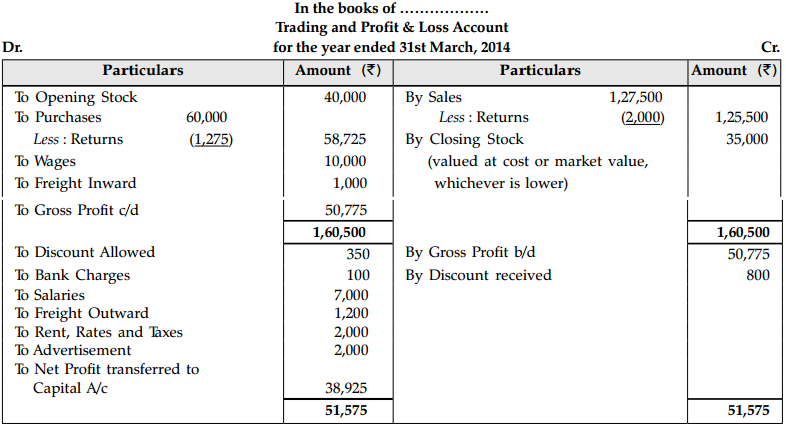

The Trial Balance shows the following balances as at 31.3.2014 :

Cost of Closing Stock ₹ 40,000; but its market value was ₹ 35,000.

Prepare Trading and Profit & Loss Account for the year ended 31.3.2014. [3]

Answer:

Question 33.

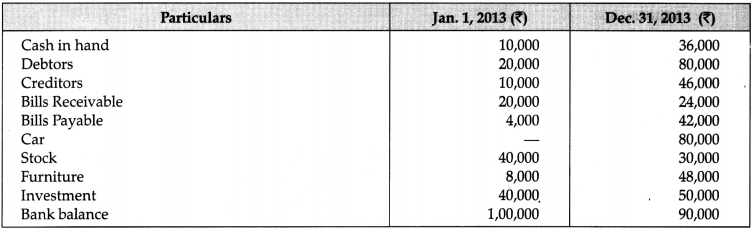

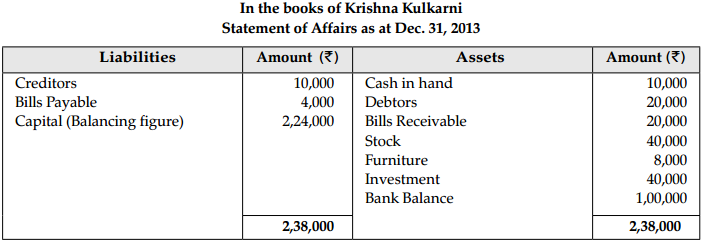

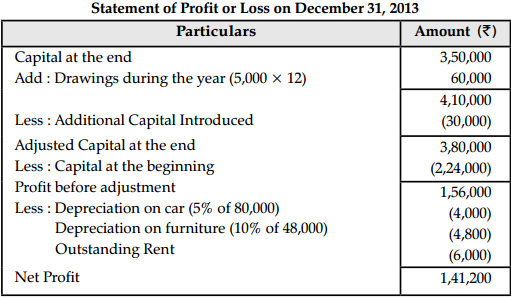

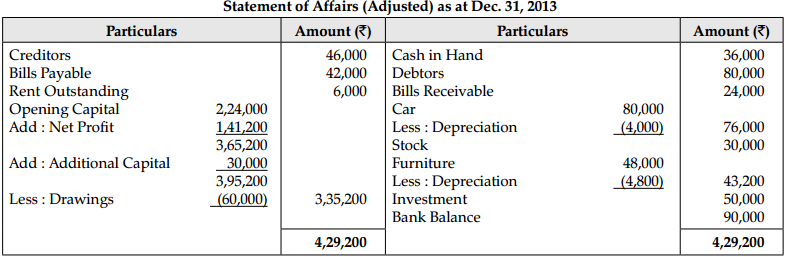

Krishna Kulkarni has not kept proper books of accounts, prepare the statement of profit or loss for the year ending December 31,2013 from the following information:

The following adjustments were made :

(i) Krishna withdrew cash ₹ 5,000 per month for private use.

(ii) Depreciation @ 5 % on car and furniture @ 10 %

(iii) Outstanding Rent ₹ 6,000.

(iv) Fresh Capital introduced during the year ₹ 30,000.

OR

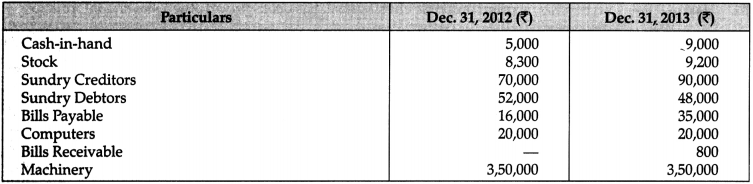

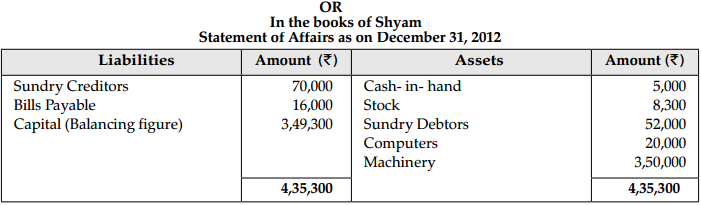

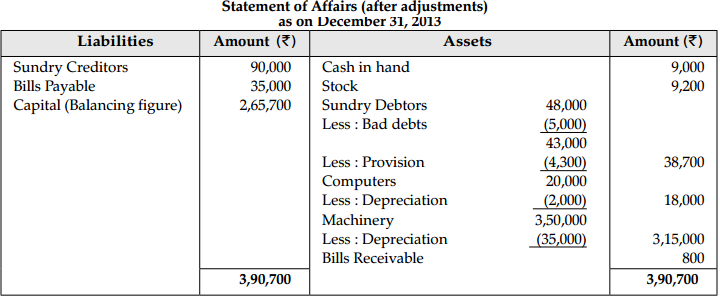

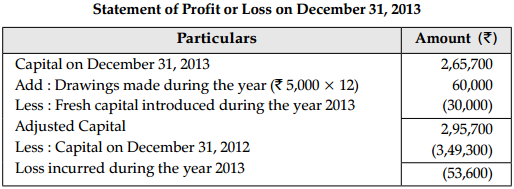

Shyam does not keep proper records. From the following information find out profit or loss and also prepare Statement of Affairs for the year ended December 31,2013.

Shyam informs about his transactions: Drawings ₹ 5,000 p.m. for personal use, fresh capital introduce during the year ₹ 30,000.

Computers and Machinery are to be depreciated @ 10% p.a. A provision of 10% is to be made on debtors for doubtful debts. It was found that ₹ 5,000 is irrecoverable from debtors. [4]

Answer:

Question 34.

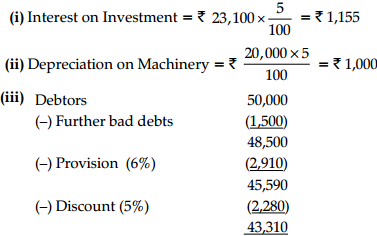

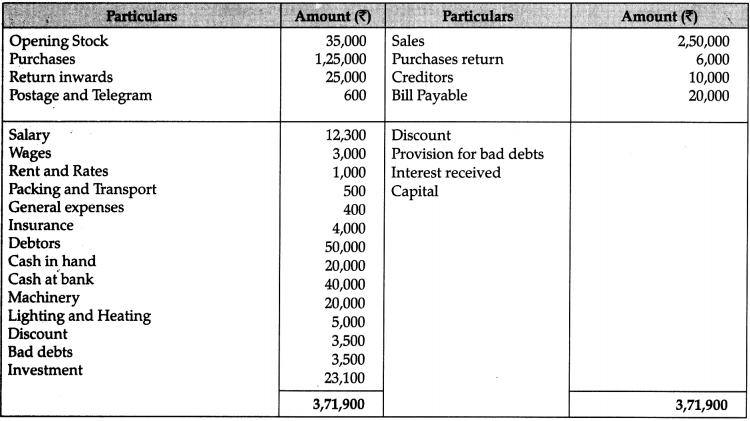

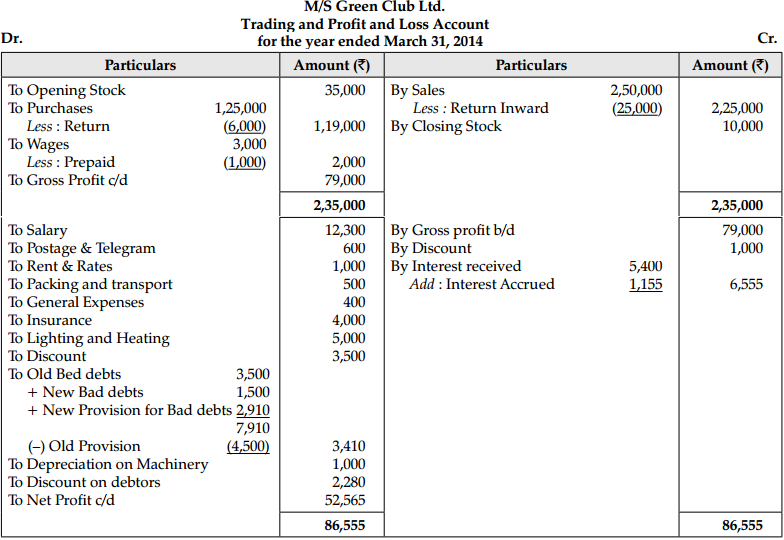

Prepare a Trading and Profit and Loss Account and Balance Sheet of M/s Green Club Ltd. year ending March 31, 2014, from the following figures taken from trial balance:

Adjustments:

(i) Depreciation charged on machinery @ 5% p.a.

(ii) Further bad debts 1,500, discount on debtors @ 5% and provision on debtors @ 6%.

(iii) Wages prepaid 1,000.

(iv) Interest on investment @ 5% p.a.

(v) Closing stock 10,000.

Answer:

Working Notes :